The infoshot to help kick-start your week

Coming up this week:

Interest rate decisions

Kevin Warsh will chair his first US Federal Reserve Committee meeting this week. With inflation at a three-year high due to soaring energy costs, and recent US job numbers beating expectations, the Fed is widely expected to leave interest rates unchanged.

The Bank of England are also expected to hold interest rates when they meet this week. On Friday the European Central Bank (ECB) raised its main deposit rate by 0.25% to 2.25%. The Bank of Japan is expected to follow suit on Wednesday and raise its interest rate by the same margin, taking it to 1%. If you want more information on Warsh’s appointment and the outlook for interest rates, I’ve recently written a longer piece on the subjects which we’ll be publishing later this week.

Last week:

US-Iran peace deal agreed

Investors drew a collective sigh of relief last night after Pakistan’s Prime Minister Shehbaz Sharif announced a deal between the US and Iran to end the conflict in the Middle East. Sharif said both sides had agreed to “the immediate and permanent termination of military operations on all fronts, including Lebanon”.

However, the situation in Lebanon could jeopardise the signing of the deal. Israel’s Defence Minister, Israel Katz, says the IDF plans to stay in Lebanon “without time limits”, whereas Iran’s Foreign Minister, Seyyed Abbas Araghchi has said today that a “complete halt” to Israeli attacks in Lebanon is required. Under the deal, the US blockade of Iranian ports will be removed, allowing the Strait of Hormuz to finally reopen. On Truth Social, Trump posted “Ships of the World, start your engines. Let the oil flow!” According to Trump the strait will reopen when the deal is signed on Friday. However, it could take weeks or months for mines to be cleared and damaged gas facilities to be repaired and transit to return to normal.

Oil prices tumbled after the announcement, falling to around $80 a barrel at the time of writing today. Asian markets reacted positively, with Japan’s leading index up nearly 5% when it closed.

SpaceX completes largest IPO in history

Elon Musk effectively became the world’s first trillionaire on Friday after SpaceX landed on the stock market and exceeded its estimated listing price by 18%. Musk’s majority ownership of class B shares also now means he’ll control over 85% of shareholder voting power. The float is expected to create 4,000 new millionaires among SpaceX’s current and former employees. Normally, early investors and employees would have to wait 180 days before selling their shares; however, they can gradually start selling (initially up to 20%) once SpaceX’s Q2 earnings get released in late July or early August. SpaceX’s valuation finished trading at $2.1tn. Widening operating losses and the AI division’s huge capital expenditure didn’t put off investors. Demand was reportedly four times oversubscribed, leading Senator Elizabeth Warren to call for the IPO to be delayed over “inaccurate or misleading accounting or valuation.”

One of the next AI-related IPO-listing firms, Anthropic, suffered a setback on Friday when its Fable 5 and Mythos 5 AI models were suspended for non-US citizens over security concerns. The ruling by the US Department for Commerce forced Anthropic to disable both models. The company said they think “the government believes it has become aware of a method of bypassing or jail breaking Fable 5”. Reports this weekend suggest rivals at Amazon tipped off the state department about the potential to bypass Fable 5’s safety and security restrictions.

UK economy contracts

The latest release from the Office for National Statistics (ONS) showed the UK economy contracted by 0.1% in April, its first contraction since August 2025. Rising energy costs caused by the conflict in the Middle East were the main downward driver as the services and construction sectors both fell. The contraction will increase the likelihood of the Bank of England keeping interest rates unchanged on Wednesday.

Notice:

For regulated financial advisers and investment professionals only, Copia does not provide financial advice, and the contents of this document should not be taken as such.

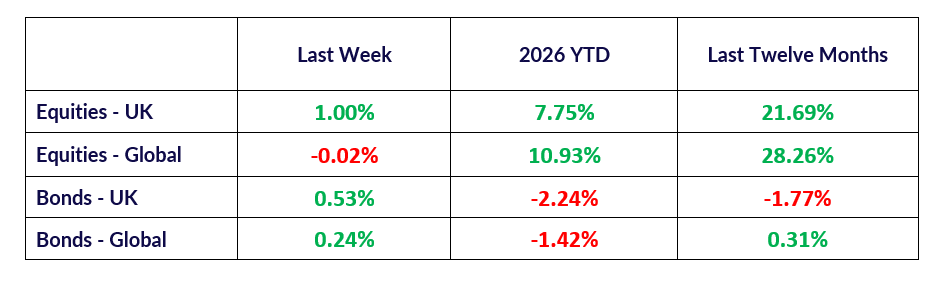

The performance of each asset class is represented by certain Exchange Traded Funds available to UK investors and expressed in GBP terms selected by Copia Capital Management to represent that asset class, as reported at previous Thursday 4:30pm UK close. Reference to a particular asset class does not represent a recommendation to seek exposure to that asset class. This information is included for comparison purposes for the period stated but is not an indicator of potential maximum loss for other periods or in the future.