The infoshot to help kick-start your week

Coming up this week:

Japan GDP and inflation data – Tuesday & Friday

The Japanese Cabinet Office is due to release Japan’s Q1 GDP data on Tuesday. Analysts are expecting to see a moderate rise largely thanks to AI sector driven growth. The impact of the energy shock caused by the war in Iran is more likely to be visible in Japan’s inflation numbers when published on Friday. Higher energy costs are expected to push up the overall inflation number although energy subsidies and the release of oil reserves should mean the impact is less significant than in other parts of Asia.

International Research Forum on Monetary Policy 2026 – Monday & Tuesday

Members of the European Central Bank (ECB) and the US Federal Reserve will meet this week in Frankfurt at the 14th edition of the International Research Forum on Monetary Policy. This year’s programme includes talks on oil shocks, fiscal policy and inflation, and wealth redistribution. This year’s keynote speech is being delivered by Italian economist Giancarlo Corsetti. He’ll be focusing on trade wars, exchange rates and monetary policy.

Last week:

US-China summit

President Trump took an entourage of top US CEOs to Beijing for the latest US-China summit. In his opening night speech at the state banquet, Trump heralded basketball and the popularity of Chinese takeaways as demonstrations of America’s deep ties to China. In quite a stark contrast, President Xi referred to the “Thucydides Trap” to issue a warning to the US about what can go wrong when an established power feels threatened by a rising power.

Trump left Beijing claiming he’d struck “fantastic trade deals, great for both countries” but no breakthroughs or business deals were officially announced. The current trade war truce that was sparked by last year’s Liberation Day tariffs is set to expire in November. President Xi is expected to visit Washington for another summit in September. How much help China has promised to provide regarding the situation in Iran is unclear, however Trump said on Friday that he will consider lifting the sanctions on Chinese firms that purchase Iranian oil.

Markets fall on Friday

Following a record-setting few days for US markets, most major indexes fell on Friday. Concerns over rising bond yields across the globe, a tech selloff, high US inflation data and elevated oil prices may all have had an impact.

30-year bond yields in the US hit their highest level in 12 months, and the UK and Japanese equivalents reached their highest levels since the late nineties. Here in the UK, concerns over the leadership of the Labour Party pushed our home bond markets (Gilts) and the pound down, and the yields on those Gilts up.

The shrinking likelihood of US Fed interest rate cuts and profit-taking caused much of the tech selloff on Friday. The US Consumer Price Index (CPI) data for April showed inflation rose 3.8% annually, the highest jump for three years. The annual rate was 0.1% ahead of expectations. Energy price rises accounted for more than 40% of the gain. The report also showed that average US hourly wages have fallen 0.3% in the last year. Kevin Warsh’s role as Fed Chair was also confirmed by the US senate last week, but with inflation going in the wrong direction it’s looking increasingly unlikely that he’ll be able to cut interest rates anytime soon.

Last night, in amongst a batch of posts containing AI-generated images, including one of himself and a topless alien, Trump took to Truth Social to threaten Iran again, “For Iran, the Clock is Ticking, and they better get moving, FAST, or there won’t be anything left of them. TIME IS OF THE ESSENCE!” In response, oil prices rose again this morning hitting Asian markets when they opened.

Notice:

For regulated financial advisers and investment professionals only, Copia does not provide financial advice, and the contents of this document should not be taken as such.

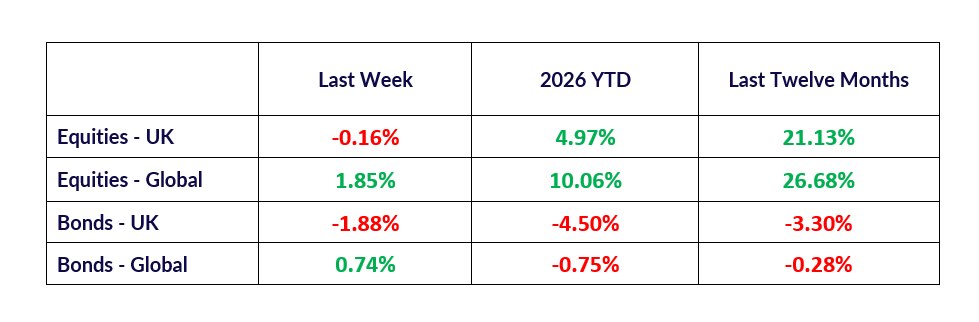

The performance of each asset class is represented by certain Exchange Traded Funds available to UK investors and expressed in GBP terms selected by Copia Capital Management to represent that asset class, as reported at previous Thursday 4:30pm UK close. Reference to a particular asset class does not represent a recommendation to seek exposure to that asset class. This information is included for comparison purposes for the period stated but is not an indicator of potential maximum loss for other periods or in the future.