The infoshot to help kick-start your week

Coming up this week:

Interest rate decisions – Tuesday to Thursday

The Federal Reserve, Bank of England, Bank of Japan and the European Central Bank will all hold meetings this week to make their latest decisions on interest rates. Across the board, no rate changes are widely expected. However, analysts and investors will have a firm eye on the statements and guidance to gauge the likelihood of rate changes later in the year and get a better grasp of the economic fallout from the conflict in Iran.

This week’s Federal Reserve meeting could be the last presided over by Jerome Powell. His likely successor, Kevin Warsh, faced some tough questioning from senators during his confirmation hearing last week. He denied Elizabeth Warren’s characterisation of him as President Trump’s “sock puppet” and said, “The president never once asked me to commit any particular interest rate decision, and nor would I ever agree to do so if he had”. Republican Senator Thom Tillis was still withholding his support due to the US Justice Department’s investigation into Jerome Powell. On Friday, it was announced that the department had dropped the investigation, potentially clearing the way for Warsh.

Mag’ 7 earnings – Wednesday & Thursday

Five of the “Magnificent Seven” tech companies report their first quarter earnings this week. Aside from earnings, the reports will also provide updates about their massive AI spending plans.

Last week:

AI helps Asian and US markets defy war

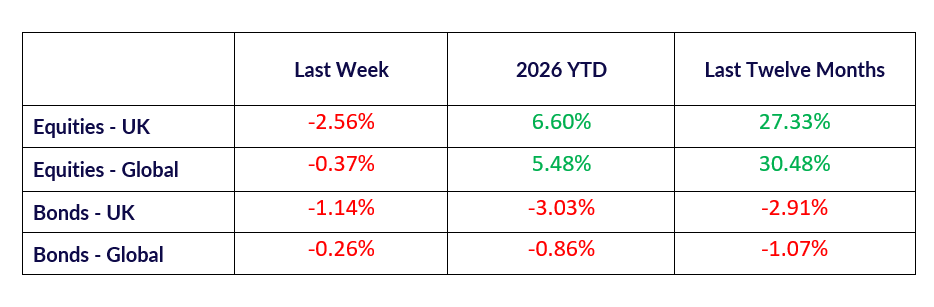

On Tuesday, Trump indefinitely extended the US’s ceasefire with Iran. During the week, Iran seized two ships, and the US continued its blockade of Iranian ports, turning thirty ships back around. Oil prices rose steadily throughout the week. However, for some markets, like the week before, AI optimism outweighed energy concerns. Japanese and South Korean markets reached record highs today. Their dominance in the semiconductor and memory chip markets has largely been behind the recent tailwinds.

US markets have fully recovered from their major slump at the end of March. 28% of large US firms have now reported their Q1 earnings, so far 84% are beating estimates.

UK updates on inflation and unemployment, BoE warning

Without a meaningful UK presence in the AI industry, the lack of progress in Iran meant UK equity markets fell last week.

The latest UK Consumer Price Inflation (CPI) from the Office for National Statistics (ONS) showed inflation rose as expected by 3.3% in March. The Iran war has caused the biggest jump in fuel prices for three years.

The UK unemployment rate unexpectedly fell to 4.9%. The fall was driven by an increase in the number of people not actively seeking work, including fewer students looking for work while studying. This meant the inactivity rate rose from 20.7% to 21%.

On Friday, the Bank of England (BoE) issued another warning about inflated stock market valuations. The bank’s Deputy Governor, Sarah Breeden warned, “There’s a lot of risk out there and yet asset prices are at all-time highs. We expect there will be an adjustment at some point.” She didn’t suggest when or by how much markets could fall but said she feared the impact of risks like private credit and the AI boom crystalising at the same time.

DeepSeek spares markets this time around

DeepSeek, the Chinese AI startup who shook up markets in January 2025, launched a preview of their new model on Friday. It didn’t disturb markets like it did last year (Nvidia actually finished the week at a record high), but the pricing is significantly cheaper than its American counterparts and it’s easier to optimise, raising questions for DeepSeek’s US rivals. That said, Tesla has announced that their capital expenditure plan for 2026 will treble in order to invest more in AI, robotaxis and robotics, and Meta will cut staff by 10% to compensate for already-announced increases in AI spending. We would expect market watchers to take a keen interest in the evolution of earnings from, and investment in, AI that will be announced by other “Magnificent Seven” companies later in the week.

Notice:

For regulated financial advisers and investment professionals only, Copia does not provide financial advice, and the contents of this document should not be taken as such.

The performance of each asset class is represented by certain Exchange Traded Funds available to UK investors and expressed in GBP terms selected by Copia Capital Management to represent that asset class, as reported at previous Thursday 4:30pm UK close. Reference to a particular asset class does not represent a recommendation to seek exposure to that asset class. This information is included for comparison purposes for the period stated but is not an indicator of potential maximum loss for other periods or in the future.