The infoshot to help kick-start your week

Attempts to contain oil prices lead to more marginal market losses

Various attempts to try and counter rising oil prices helped keep the price of oil below $100 a barrel in the early stages of last week. On Monday, South Korea and Thailand said they would set limits on fuel prices. All 32 members of the International Energy Agency (IEA) agreed to release a record 400 million barrels of oil from their emergency reserves. Despite this being more than double the amount released in 2022 following Russia’s invasion of Ukraine, it still only constitutes two weeks’ worth of what would normally pass through the Strait of Hormuz.

Saudi Arabia’s state oil firm, Aramco, warned of “catastrophic consequences” for oil markets if Hormuz remains blocked. This weekend, President Trump called on his allies to help “take care of that passage” and warned that Nato faces a “very bad” future if its members fail to assist. So far, none of the world’s leading economies have committed to supporting the US in the Strait. The UK is considering sending aerial minesweepers to help clear the waterway of mines.

The Centre for Research on Energy and Clean Air (CREA) estimated last week that Russian oil, gas and coal sales have so far climbed by more than 10% in March. On Friday, Trump eased some sanctions on countries buying Russian oil. Allowing Russia to sell more oil is unlikely to have much impact on oil price pressures. Russia claims to have 100 million barrels of oil at sea which is less than a single day’s global demand for oil (104 million barrels). With Hormuz still effectively shut and the Iranian military vowing to “not allow a single litre of oil to transit”, oil prices have gone back above $100 a barrel today.

The downward effect of the conflict on markets was less dramatic than the week before. Expect inflations fears to dominate the notes from this week’s Fed and Bank of England (BoE) interest rate meetings.

GDP data from UK, US and Japan

The latest figures from the Office for National Statistics (ONS) showed the UK economy unexpectedly flatlined to 0% growth in January. Lower than many analysts’ expectations of 0.2% growth, the pound fell against the dollar and UK bond yields rose on the news. With UK unemployment at a five-year high, the ONS attributed the fall in employment activities as the largest negative contributor to January’s GDP numbers.

Across the pond, the latest release from Bureau of Economic Analysis (BEA) showed US GDP grew by 0.7% in the fourth quarter of 2025. 0.7% is well below the previous estimate of 1.4% and the Dow Jones forecast of 1.5%. According to the BEA, less services spending, particularly in healthcare, caused the largest downward drag on the GDP numbers.

Japan’s GDP growth for the fourth quarter of 2025 was revised to 1.3% marking a strong turnaround from Q3’s -2.6% contraction. Strong business spending and private consumption were behind the bounce back. So far, rising oil prices have had a limited impact on inflation due to the abolishment of the provisional gasoline tax rate at the end of last year, and government subsidies to petrol companies to help stabilise prices.

Chinese markets buoyed by OpenClaw popularity

Chinese markets saw a bit of a boost last week as investors reacted to the surging popularity of OpenClaw in the country and the potential to monetise returns from its AI software. Many of China’s biggest cloud providers like Alibaba Cloud and Baidu, have all started incorporating OpenClaw’s AI agents and floods of startups have released their own “Claw” frameworks. OpenClaw’s software aligns well with China’s embrace of open-source AI technology and with subscriptions rising, some investors are excited that it might represent a way forward for generating actual revenue from AI software.

On Wednesday, Meta bought the AI social media network, Moltbook for an undisclosed price as they continue competing with the likes of OpenAI and Google to secure more partnerships with leading AI startups.

Coming Up:

- Fed interest rate decision, Wednesday 18 March 2026

- Bank of Japan (BoJ) interest rate decision, Thursday 19 March 2026

- Bank of England (BoE) interest rate decision, Thursday 19 March 2026

Notice:

For regulated financial advisers and investment professionals only, Copia does not provide financial advice, and the contents of this document should not be taken as such.

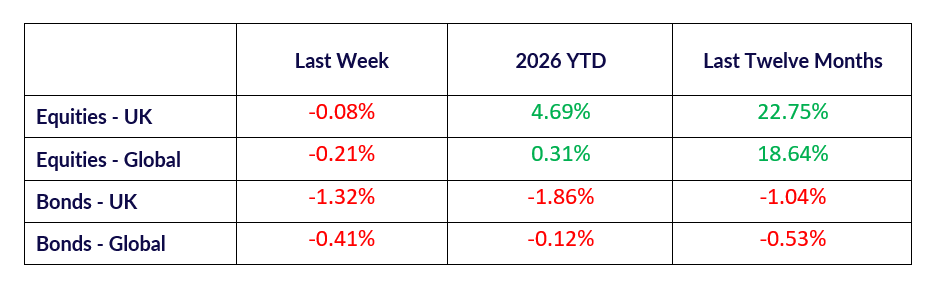

The performance of each asset class is represented by certain Exchange Traded Funds available to UK investors and expressed in GBP terms selected by Copia Capital Management to represent that asset class, as reported at previous Thursday 4:30pm UK close. Reference to a particular asset class does not represent a recommendation to seek exposure to that asset class. This information is included for comparison purposes for the period stated but is not an indicator of potential maximum loss for other periods or in the future.