The infoshot to help kick-start your week

AI claims more victims in latest market selloff

Fresh fears over new AI innovations hit the UK and US wealth management sectors last week. On Monday, US startup, Altruist unveiled a new AI driven tax planning tool which they claim can “produce fully personalised tax strategies… in minutes.” The latest feature from their Hazel AI platform can supposedly generate personalised tax strategies for advisers that use scenario modelling to assess the impact of increased income, lifestyle changes and retirement on a client’s plans. The potential for tools like this to serve more clients more efficiently led to a market selloff in the wealth management sector that was similar to the previous week’s software exodus. In the UK, shares in St James’s Place, AJ Bell and Quilter all fell. Big names in the US like, Charles Schwab and Raymond James also declined.

Shares in price comparison site owners, Mony Group and Future also tumbled after the US firm, Insurify, launched a new service that allows users to compare car insurance quotes using Open AI’s ChatGPT.

This weekend’s big AI development was the announcement last night that OpenClaw founder, Peter Steinberger is joining OpenAI. Previously called Clawdbot and Moltbot, OpenClaw provides AI agents that can ‘autonomously’ complete tasks, like coding or workflow automations, without constant prompts and oversight from humans.

Just in: ups and downs in latest US jobs data

On Wednesday the latest US jobs data from the Bureau of Labor Statistics showed the US added 130,000 jobs in January. It was primarily driven by the healthcare and construction sectors. The uplift was nearly double what many analysts had expected. President Trump took to Truth Social to celebrate, “Just in: GREAT JOBS NUMBERS, FAR GREATER THAN EXPECTED… The Golden Age of America is upon us!!!”

However, it wasn’t all good news, as the report also contained a major revision to 2025’s overall new jobs total. According to the latest data, the total number of new jobs for 2025 was 181,000. That’s down markedly from the initially reported estimate of 584,000. The revision means last year’s job growth was actually the lowest since Covid, and far lower than the 2 million jobs that were added in 2024. The revised number is more in line with the downward trend in US job openings. The Bureau’s recent Jolts report showed openings had fallen by 386,000 in December and also reached their lowest level since Covid.

Released on Tuesday, a new report on household debt by the Federal Reserve Bank of New York showed US credit card debt rose by 5.5% in the last twelve months. This takes the total of outstanding balances up to $1.28tn. According to debt management company Achieve, 55% of US consumers are currently using credit cards to cover essential expenses and necessities.

UK and Japan GDP data

Figures from the Office for National Statistics (ONS) showed the UK economy grew by only 0.1% in the final quarter of last year. According to Liz McKeown, the Director of Economic Statistics at the ONS, “The often-dominant services sector showed no growth, with the main driver instead coming from manufacturing. Construction, meanwhile, registered its worst performance in more than four years.” The overall economic growth figure for 2025 came out at 1.3%, worse than the official forecasts of 1.5% but better than the 1.1% growth in 2024.

Sunday’s data from the Economic and Social Research Institute showed Japan narrowly avoided a technical recession after its economy grew by 0.1% in the final quarter of 2025. Private consumption offset low exports and lower spending on public services. With many analysts expecting an expansion of 0.4%, the Japanese Yen and the Nikkei 225 fell slightly in response.

Coming Up:

- German CPI, Tuesday 17 February 2026

- GB CPI, Wednesday 18 February 2026

- US GDP (Q4), Friday 20 February 2026

Notice:

For regulated financial advisers and investment professionals only, Copia does not provide financial advice, and the contents of this document should not be taken as such.

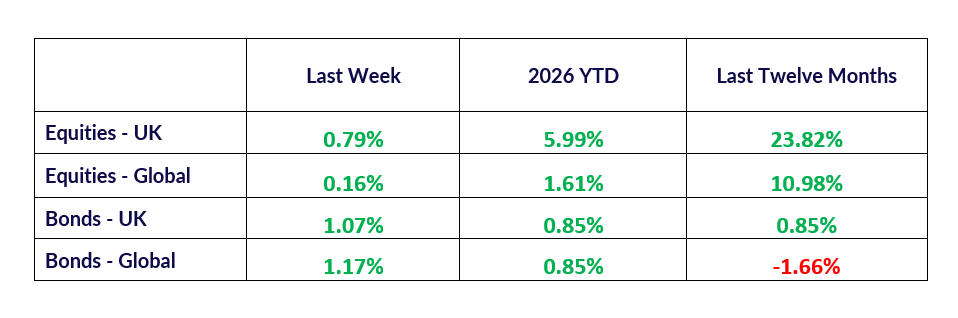

The performance of each asset class is represented by certain Exchange Traded Funds available to UK investors and expressed in GBP terms selected by Copia Capital Management to represent that asset class, as reported at previous Thursday 4:30pm UK close. Reference to a particular asset class does not represent a recommendation to seek exposure to that asset class. This information is included for comparison purposes for the period stated but is not an indicator of potential maximum loss for other periods or in the future.