The infoshot to help kick-start your week

Gains in US markets as rate cut this week looks more likely

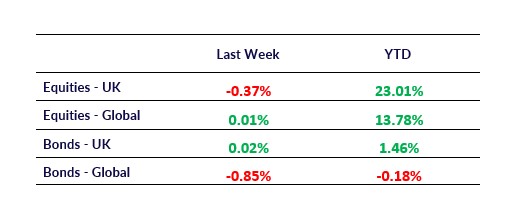

US markets made modest gains last week as the odds of an interest rate cut happening at this week’s Federal Reserve meeting increased. Wednesday’s data from payroll processing firm ADP showed private employers in the US shed 32,000 jobs in November. ADP’s Chief Economist, Nela Richardson said the fall was “led by a pullback among small businesses” as small firms (less than 50 employees) removed 120,000 jobs in total. With the next batch of shutdown-delayed government jobs data not due until after the next Fed meeting, the ADP numbers will add more pressure on the Fed to cut rates on Wednesday.

Oil prices reached a two-week high today in anticipation of a rate cut that might stimulate economic activity and boost the demand for fuel. The slow progress of Ukraine-Russia peace talks and tensions between the US and Venezuela are also impacting the oil price. Despite only exporting around 1% of consumed oil, Venezuela has the world’s largest oil reserves and regime change following a US intervention would have a major impact on prices and the oil trade. The Americans have heavily built up their military resources in the region since September. They’ve deployed the world’s largest aircraft carrier, the USS Gerald R. Ford, and, according to estimates by the Washington Post, now have 10,000 troops and 6,000 sailors stationed in the Caribbean.

New economic data from Europe and Japan

Indexes across the Eurozone also posted small gains. The European Commission released the latest inflation, GDP and employment data last week. Inflation rose from 2.1% in November to 2.2%, and in the last quarter GDP increased by 0.3%. Employment also ticked up 0.2%.

This morning, the final GDP data from before Sanae Takaichi’s appointment as PM, showed Japan’s GDP fell 0.6% in the last quarter (July to September), worse than the expected decline of 0.4%. Investors will be keeping a keen eye on upcoming economic data releases to see if Takaichi’s stimulus measures help boost the economy. On Thursday, the yields on Japanese governments bonds reached their highest level since 2007. They’ve climbed again today, and the 10-year yield now sits at 1.975%.

Netflix agrees to buy Warner Bros in $83 blockbuster deal

Netflix agreed to buy the film and streaming parts of Warner Bros Discovery on Friday. They beat Comcast and Paramount Skydance to secure the entertainment business. The board of directors at both firms unanimously agreed the deal but it is likely to face a legal challenge from rival bidder Paramount. Trump, who is close friends with Paramount’s Larry Ellison, confirmed he will get involved in the government’s decision to approve the takeover and said the companies’ combined size “could be a problem”. And as of this afternoon, Paramount have now made a counteroffer of $108.4bn for the whole business as they try to scupper the deal by appealing directly to shareholders.

Meta shares rose after they announced plans to cut up to 30% from their Metaverse budget as they shift more funding towards AI development. They also struck AI data agreements with several news publishers to enable their AI chatbot to provide “real-time” news from a variety of sources. In other AI publishing news, Waterstones’ CEO James Daunt said his bookstores would stock books created by AI if customers wanted them and they were clearly labelled. This weekend he said, if an AI produced the next War and Peace, “if people want to read that book, AI generated or not, we will be selling it – as long as it doesn’t pretend to be something that it isn’t.” Of course, as we’ve seen recently with the launch of AI TikTok rival, Sora, there remains a question mark over the appetite for AI curated or created media content.

Coming Up:

- US job openings (October), Tuesday 9 December 2025 at 15:00

- Fed interest rate decision, Wednesday 10 December 2025 at 19:00

- UK GDP (October), Friday 12 December at 07:00

Notice:

For regulated financial advisers and investment professionals only, Copia does not provide financial advice, and the contents of this document should not be taken as such. The performance of each asset class is represented by certain Exchange Traded Funds available to UK investors and expressed in GBP terms selected by Copia Capital Management to represent that asset class, as reported at previous Thursday 4:30pm UK close. Reference to a particular asset class does not represent a recommendation to seek exposure to that asset class. This information is included for comparison purposes for the period stated but is not an indicator of potential maximum loss for other periods or in the future.