The infoshot to help kick-start your week

More poor UK job numbers, CEO pay reaches an all-time high

The number of people in work in UK fell for a sixth consecutive month in July, down by 8,000. June’s decline was revised from 41,000 to 26,000, as the Office for National Statistics (ONS) warned that payroll numbers should be treated with caution following concerns about the quality of the data.

Vacancies tumbled again by 44,000 to 718,000. ONS Director of Economic Statistics, Liz McKeown said the latest numbers “point to a continued cooling of the labour market” and that the fall in the number of employees on payroll this year has been “concentrated in hospitality and retail.” Increases to the minimum wage and employer NI contributions combined with inflation have contributed to the decline in both sectors. Average earnings growth (excluding bonuses) remained at 5%.

At the top end of the workforce, analysis released by the High Pay Centre showed that CEO pay for FTSE 100 bosses has now reached an all-time high. The median pay for a CEO increased 7% to £4.58mn, 122 times the salary of the average UK full-time employee.

There was better news for UK GDP as it went up 0.4% in June after contracting 0.1% in May. Growth in services, industrial output and construction were behind the increase.

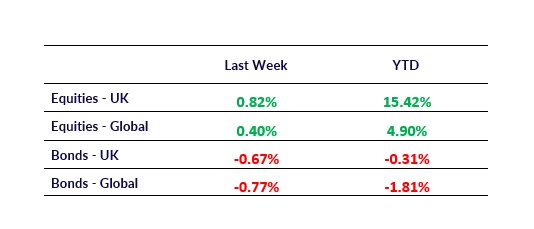

The FTSE 100 broke another market record reaching 9,222 at the start of trading on Friday. Mining companies led the charge due to the increase in copper prices and improved chances of a US Fed rate cut in September.

Before wooing Putin, Trump does some deal making with chip manufacturing giants

Before wooing and rolling out the red carpet for Vladimir Putin, Trump did some important deal making with computer chip manufacturing giants Nvidia and AMC. The deal would loosen export restrictions allowing both firms to sell currently banned chips to China, in return for the companies giving the US government 15% of any sales revenue. A downgraded version of Nvidia’s new “super-duper advanced” chip, the Blackwell, could be exportable under the new deal.

US equity markets had another good week with small-cap stocks doing particularly well. On Tuesday, they benefited from the US Consumer Price Index (CPI) beating expectations by holding at 2.7% for July and increasing the chances of a Fed rate cut in September. However, the latest US Producer Price Index (PPI) numbers released after will have dented some of this optimism as they demonstrated a 0.9% inflation surge, taking the PPI level to its highest since March 2022. The disparity between the CPI and PPI could be down to consumers cutting back on spending while Trump’s tariffs drive up business costs.

Chinese stocks rally following 90-day pause on higher tariffs

Stock markets in China did well after Beijing and Washington agreed to extend the tariff pause on each other’s goods until November. The tariff hike was set to take effect this week. The extension will hopefully give both parties the time to normalise trade relations and reach a sustainable long-term agreement.

Japanese markets also responded positively on the back of this news. The US-China tariff pause extension, plus a strong corporate earnings season and a weaker yen provided the Nikkei with the momentum to reach a record high of 43,714 points when the market closed today.

Coming Up:

- UK CPI July, Wednesday 20 August 2025 at 07:00am

- German GDP Q2, Friday 22 August 2025 at 07:00am

- Fed Chair speaks, Friday 22 August 2025 at 15:00pm

Notice:

For regulated financial advisers and investment professionals only, Copia does not provide financial advice, and the contents of this document should not be taken as such. The performance of each asset class is represented by certain Exchange Traded Funds available to UK investors and expressed in GBP terms selected by Copia Capital Management to represent that asset class, as reported at previous Thursday 4:30pm UK close. Reference to a particular asset class does not represent a recommendation to seek exposure to that asset class. This information is included for comparison purposes for the period stated but is not an indicator of potential maximum loss for other periods or in the future.