The infoshot to help kick-start your week

All roads lead to LA

The entirely predictable bust-up between the world’s most powerful man and the richest, finally happened in very public fashion on Thursday. Upset about Trump’s “big, beautiful” tax and spending bill and the $2.4tn it would add to US debt, Musk called for Trump to be impeached, claimed the Epstein files weren’t being released because Trump features in them, and suggested starting a new political party “that actually represents the 80% in the middle”.

Trump responded by threatening to tear up Musk’s US government contracts. Musk’s net worth fell $33bn on Thursday with Tesla shares dropping 14% on the day. Tesla shares did recover 6% on Friday when it became clear that Musk was willing to back down in the dispute. In another predictable and worrying development, this weekend Trump reacted to protests over raids conducted by ICE officers in Los Angeles by deploying 2,000 National Guard troops to the city. Gavin Newsom, the Governor of California, has labelled the deployment as “purposefully inflammatory”.

Meta going nuclear to power AI

On Tuesday, Meta signed a contract with Constellation Energy to keep it’s Illinois nuclear reactor operating for 20 years. Large tech companies have been looking to secure electric power sources as their demand for energy rises drastically due to the needs of data centres and AI. Google reached a similar deal with California’s Kairos Power last year.

Anonymous sources told the Wall Street Journal that Meta expects all advertisers to be able to “fully create and target ads” using AI by the end of the next year. AI will be able to personalise ads in real time based on a user’s location and all the millions of other factors that get scooped into Meta’s various algorithms. Advertising made up 97% of Meta’s revenue last year.

Also, this morning, Bloomberg is reporting that Meta is in talks to invest $10bn in Scale AI. The AI data labelling start-up already plays a crucial role in training machine-learning models for Microsoft and OpenAI.

ECB cuts rates to 2% as steel tariffs climb to 50%

Back in Europe, the European Central Bank trimmed its deposit rate to 2%, it’s lowest level since 2022. The move was widely expected and came with only one policymaker dissenting.

Economic growth has slowed across the eurozone, and the outlook for next year is weak according to EU forecasts. The ECB will be hoping that the move will boost economic growth as it tackles the damage caused by Trump’s tariffs. As scheduled, US tariffs on steel and aluminium imports rose to 50% on Wednesday. The increase applies to all trading partners except the UK where the rate will remain at 25% until at least 9 July.

China’s factory output plunges

According to the latest private Caixin China General Manufacturing PMI survey, activity in May fell at its fastest pace since September 2022. The decline in demand for foreign goods accelerated in May leading to new orders falling to their lowest level since July 2023.

The data shows the impact Trump’s tariffs are having on Chinese exporters and there is likely to be renewed calls for Beijing to roll out more measures or stimulus to help offset the impact while a broader trade agreement is being negotiated.

Coming Up:

- US 10-year bond auction, Wednesday 11 June 2025 at 18:00pm

- US 30-year bond auction, Thursday 12 June 2025 at 18:00pm

- German CPI, Friday 13 June 2025 at 07:00am

Notice:

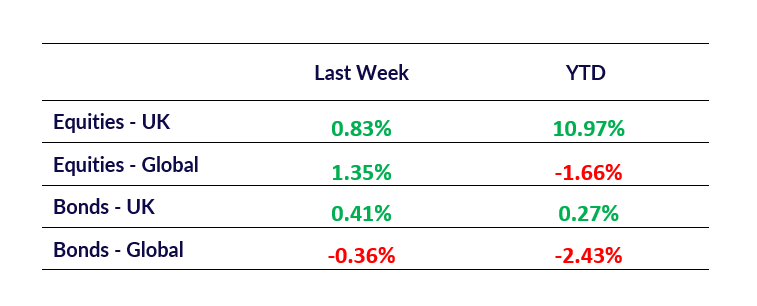

For regulated financial advisers and investment professionals only, Copia does not provide financial advice, and the contents of this document should not be taken as such. The performance of each asset class is represented by certain Exchange Traded Funds available to UK investors and expressed in GBP terms selected by Copia Capital Management to represent that asset class, as reported at previous Thursday 4:30pm UK close. Reference to a particular asset class does not represent a recommendation to seek exposure to that asset class. This information is included for comparison purposes for the period stated but is not an indicator of potential maximum loss for other periods or in the future.