The infoshot to help kick-start your week

IMF slashes global growth forecasts

On Tuesday the International Monetary Fund (IMF) published the latest edition of its World Economic Outlook. The IMF said Trump’s tariffs have been a “major negative shock” to the world economy as they slashed their forecasts for growth around the world.

Global GDP growth was cut from the 3.3% forecasted in January to 2.8%. The UK growth forecast fell from 1.6% to 1.1%, and the US has deteriorated from 2.7% to 1.8%. Even after Trump paused many of his “reciprocal tariffs”, the IMF said trade barriers were at the highest level in a century. The IMF expects companies across the globe to respond to the present situation by cutting spending, and they’ve raised the probability of a recession in the US to 40%.

Backtracking from Trump leads to a better week for US markets

As Trump approached his 100th day back in office, there were signs that he might be willing to retreat on his China tariffs saying on Tuesday that they will “come down substantially – but it won’t be zero”. He also seems to have had a change of heart regarding Fed Chair Jerome Powell, where within days Powell went from being a “major loser” whose “termination cannot come fast enough” to someone Trump has “no intention of firing”. His comments on China and Powell helped kick off a better week on Wall Street where the S&P 500 index climbed 4.6%.

The latest US house sales data was released on Wednesday and Thursday. House sales of existing homes declined by 5.9% in March, the steepest monthly drop since November 2022. New home sales on the other hand, increased by 7.4% in March, way beyond previous expectations as buyers look to take advantage of a fall in mortgage rates.

Following a 70% fall in Telsa profits and accusations that Elon Musk has taken his focus off Telsa, Musk announced that his time allocation to the Department of Government Efficiency (DOGE) will drop significantly from May.

Trade discussions ongoing as Japan announces tariff relief package

The prospect of trade tensions easing boosted Japanese markets last week with the Nikkei index gaining nearly 3%. More bilateral trade discussions between Japan and the US took place but a quick deal has been ruled out, and reports suggest the US have been unable to clearly articulate what they want during negotiations.

According to some current and former government officials, Japan intends to push back against any US efforts to start an economic bloc aligned against China. On Friday, Japan’s government announced a series of emergency economic measures to counter the impact of US tariffs. The relief package includes reducing the price of fuel, partially covering electricity bills and more low-interest loans for smaller companies.

Back in Europe, Bundesbank President, Joachim Nagel said on Wednesday that the German economy could suffer “a slight recession” this year, contracting for a third consecutive year for the first time.

Germany’s export focussed economy is highly vulnerable to the effects of its biggest trading partner’s tariffs, and the German government has cut its growth forecast from 0.3% to a period of stagnation.

Coming Up:

- US GDP Q1 Data, Wednesday 30 April 2025 at 13:30pm

- Japan BOJ Rate Decision, Wednesday 30 April 2025 at 04:00am

- US Unemployment Rate, Friday 2 May 2025 at 13:30pm

Notice:

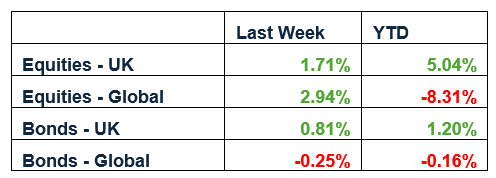

For regulated financial advisers and investment professionals only, Copia does not provide financial advice, and the contents of this document should not be taken as such. The performance of each asset class is represented by certain Exchange Traded Funds available to UK investors and expressed in GBP terms selected by Copia Capital Management to represent that asset class, as reported at previous Thursday 4:30pm UK close. Reference to a particular asset class does not represent a recommendation to seek exposure to that asset class. This information is included for comparison purposes for the period stated but is not an indicator of potential maximum loss for other periods or in the future.