The infoshot to help kick-start your week

Cash ISA review delayed as Reeves prepares for Wednesday’s Spring Statement

February’s UK public finance data, published on Friday, showed the government borrowed £10.7bn. That’s £4.2bn more than the Office for Budget Responsibility had estimated, and the fourth highest borrowing for a February since records began in 1993 (the three others occurred during the global financial crash and covid).

The figures may make the UK chancellor, Rachel Reeves, even more convinced she needs to act during Wednesday’s Spring Statement. Despite this, it looks like any changes to cash ISAs are on hold for now. Reported early last week, Reeves is no longer planning to announce any changes to cash ISA limits in Wednesday’s Spring Statement. The widely circulated plans of possibly reducing the limit to £4,000 to encourage savers to invest in equities, are not off the table and could come later in the year as part of a wider package to reform ISAs. On Sunday, it was confirmed that there are ongoing discussions about the UK’s £1bn a year digital service tax. However, any decisions on the tax, which effects big tech firms like Meta, Alphabet and Amazon, may not be made in time for this week’s Spring Statement.

As was widely expected, the Bank of England held interest rates at 4.5% on Thursday, with the nine-person Monetary Policy Committee voting 8-1 in favour of holding, with the one-member voting against arguing for a cut. The decisive vote could be seen as a sign that rates will remain at 4.5% for a while, but no one can be certain.

In the markets, travel and airline stocks fell on Friday after Heathrow Airport cancelled more than 1,000 flights due to a fire at its substation in Hayes, West London.

Fed leaves rates unchanged as ‘reciprocal’ tariffs draw nearer

On Wednesday, the Federal Open Market Committee kept its target borrowing rate between 4.25%-4.5%. Despite the uncertain impact of Trump’s tariffs, DOGE layoffs and tax breaks, the fed still expects to make another half percentage point cut through two reductions later in the year.

With 2nd April drawing nearer, there was some hope last week that the scope of Trump’s tariffs may be narrower than first feared. Trump himself stated there will be some “flexibility” as it looks like all the ‘reciprocal’ tariffs will not be implemented at once. This, combined with the Fed’s decision, meant the US markets finished the week slightly up, despite earnings warnings from corporate giants Nike and FedEx.

Across the border, Canada’s newly appointed Prime Minister Mark Carney has called for a snap election to take place on 28 April 2025.

Arrest of Istanbul mayor and five nights of protest rock the Borsa

Stocks in Turkey plummeted last week after five nights of protest in response to the arrest of the Istanbul Mayor and leader of the opposition party, Ekrem Imamoglu.

The Turkish market regulator moved to ban short selling across stocks and relaxed share buyback rules in an attempt to prevent further losses. The central bank also raised interest rates in an unscheduled meeting on Thursday as the Turkish Lira tumbled, and the banking stock’s index posted its biggest weekly drop since 2001.

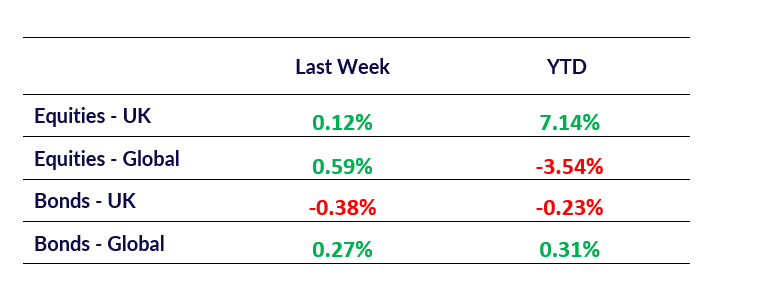

Market Pulse

Coming Up

- US CB consumer confidence, Tuesday 25th March 2025 at 10:00am.

- UK Spring Statement, Wednesday 26th March 2025 at 12:30pm.

- US Initial Jobless Claims, Thursday 27th March 2025 at 08:30am.

Notice:

For regulated financial advisers and investment professionals only, Copia does not provide financial advice, and the contents of this document should not be taken as such. The value of investments can increase and decrease, past performance and historical data cannot guarantee future success, and any references to individual stocks or asset classes are made purely for illustrative purposes. The performance of each asset class is represented by certain Exchange Traded Funds available to UK investors and expressed in GBP terms selected by Copia Capital Management to represent that asset class, as reported at previous Thursday 4:30pm UK close. Reference to a particular asset class does not represent a recommendation to seek exposure to that asset class. This information is included for comparison purposes for the period stated but is not an indicator of potential maximum loss for other periods or in the future.