The infoshot to help kick-start your week

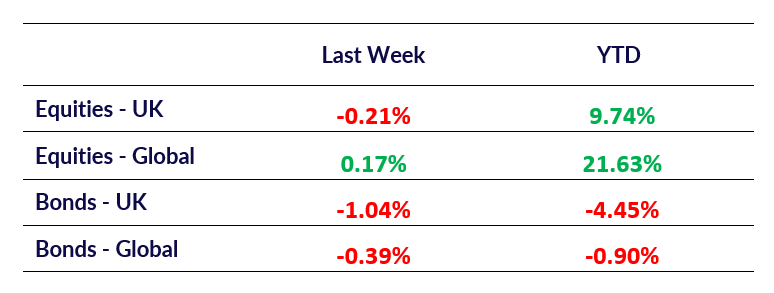

Last Week

- Chinese stocks saw their sharpest decline in three weeks as investors awaited detailed fiscal stimulus measures following the Central Economic Work Conference (CEWC). The CSI 300 index fell 2.4%, erasing recent gains, while Hong Kong-listed Chinese stocks dropped over 2%. Commodities such as iron ore and copper, reliant on Chinese demand, also slumped, reflecting market scepticism about the government’s economic pledges. The CEWC emphasised boosting consumption and domestic demand, with plans to raise the fiscal deficit and strengthen the social safety net. However, specific policies, including growth targets, remain deferred until March, leaving investors cautious. Analysts note Beijing’s reactionary policy approach, constrained by external uncertainties such as US tariffs. The market’s muted response underscores challenges in restoring confidence after prior unfulfilled promises. While additional fiscal and monetary easing is expected, a lack of immediate clarity continues to weigh on sentiment, highlighting the need for concrete, actionable measures.

- Data released by the ONS on Friday revealed that the UK economy contracted by 0.1% in October, following a similar decline in September, raising concerns about Labour’s pledge to boost growth. This marks the second consecutive monthly contraction, with GDP shrinking by 0.1% overall since Labour took office in July. Analysts warn the economy may shrink in the fourth quarter, with services stagnating and declines in manufacturing and construction output. Consumer-facing sectors, including pubs and restaurants, saw a 0.6% drop, reflecting households’ tightening budgets amid inflation concerns. A Bank of England survey found consumer inflation expectations rising to 3%, the first increase in a year. Sterling weakened, and markets priced in potential interest-rate cuts in 2025. Labour’s ambitious growth goals face challenges from cooling job markets, rising costs, and potential global trade tensions. Economists predict steady but modest growth ahead, though budget uncertainties and tax burdens could hinder progress. Chancellor Rachel Reeves acknowledged the disappointing figures, reaffirming the government’s commitment to improving living standards.

- Pimco and Fidelity are among multiple investors warning that Europe’s worsening economic outlook may force the European Central Bank (ECB) to cut rates more aggressively than markets anticipate. Current pricing suggests the ECB will lower its key rate to 1.75% in 2025, but Fidelity predicts a potential drop to 1.5%, while Pimco highlights risks of even steeper reductions. European debt markets, already outperforming US Treasuries and UK gilts this year, could rally further if rates fall faster than expected. Political instability in major eurozone economies, weak manufacturing and services sectors, and the potential impact of Donald Trump’s trade policies add to the bleak outlook. Germany, the region’s economic engine, faces a second consecutive year of contraction. Despite Thursday’s rate cut to 3%, ECB President Christine Lagarde’s less dovish tone initially unsettled markets. However, the ECB’s revised projections, coupled with a shift away from restrictive policy language, signal further easing may be on the horizon. Analysts see room for rates to fall as low as 0.5% if conditions deteriorate further.

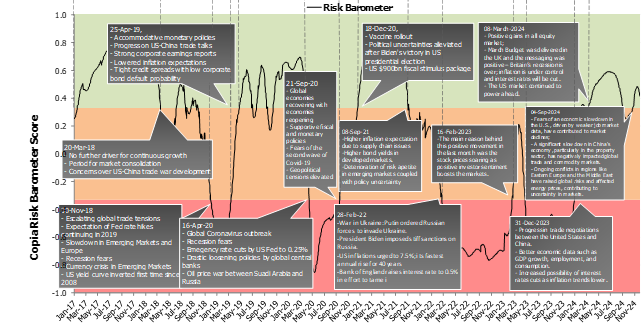

Market Pulse

Coming Up

- UK CPI Data, Wednesday 18th December 2024 at 7:00am

- US FOMC Economic predictions and interest rate decision, Wednesday 18th December 2024 at 7:00pm

- UK BOE interest rate decision, Thursday 19th December 2024 at 12:00pm

Notice:

For professional advisers only, Copia does not provide financial advice, and the contents of this document should not be taken as such. The performance of each asset class is represented by certain Exchange Traded Funds available to UK investors and expressed in GBP terms selected by Copia Capital Management to represent that asset class, as reported at previous Thursday 4:30pm UK close. Reference to a particular asset class does not represent a recommendation to seek exposure to that asset class. This information is included for comparison purposes for the period stated, but is not an indicator of potential maximum loss for other periods or in the future.Open document settingsOpen publish panel