The infoshot to help kick-start your week

Last Week

- An estimated 20,000 farmers and their families gathered in Westminster to protest Labour’s proposed “tractor tax” and inheritance tax changes announced in the recent Budget. The rally, which included well-known figures like Jeremy Clarkson, saw farmers from across the UK travel to London, filling Whitehall and Parliament Square. The National Farmers’ Union (NFU) warns that the inheritance tax reforms—limiting 100% relief on agricultural and business property to the first £1 million—could force farms to be broken up or sold. Farmers argue that this policy threatens food production and rural livelihoods. The demonstration highlighted widespread concerns about the potential economic impact on family farms, urging MPs to reconsider the proposed changes.

- The UK inflation rate rose to 2.3% in October, its highest in six months, though significantly lower than the peak of 11.1% two years ago. While inflation is stabilising, the cost-of-living crisis persists, with prices for goods and services 24% higher than in 2020, particularly impacting food and energy costs. Wages are rising faster than inflation, but concerns remain for those on benefits, set to increase by only 1.7% in April. Inflation remains volatile, driven by global factors like energy prices. Analysts caution against overreacting to one-month data, emphasising broader trends. Interest rate cuts, key to controlling inflation, are expected to be gradual. The Bank of England recently reduced the base rate to 4.75%, but further cuts may be delayed. This affects mortgage rates, which have risen slightly, while savers may benefit from stable returns. Future inflation trends are uncertain, influenced by global events and domestic policies, with potential impacts from geopolitical shifts and Budget measures.

- At COP29 in Azerbaijan, wealthier countries agreed to contribute $300 billion annually by 2035 to help developing nations cope with climate change. While this is significant, it falls short of the $1.3 trillion experts estimate is needed yearly. Critics, including India and Nigeria, called the sum insufficient, highlighting ongoing concerns about fair climate financing. The funds are earmarked for climate adaptation—such as resilient infrastructure and sustainable agriculture—and transitioning to renewable energy. However, experts stress that the agreement’s success depends on prompt and full payments from governments, international banks, and private investors. Additionally, COP29 introduced global carbon market rules, facilitating carbon credit trading to help countries meet climate targets more efficiently. By February 2025, countries must submit updated Nationally Determined Contributions (NDCs) outlining emissions reductions. Brazil’s COP30, dubbed the “COP of COPs,” aims to push for stronger commitments, emphasising the urgency of keeping the 1.5°C target within reach.

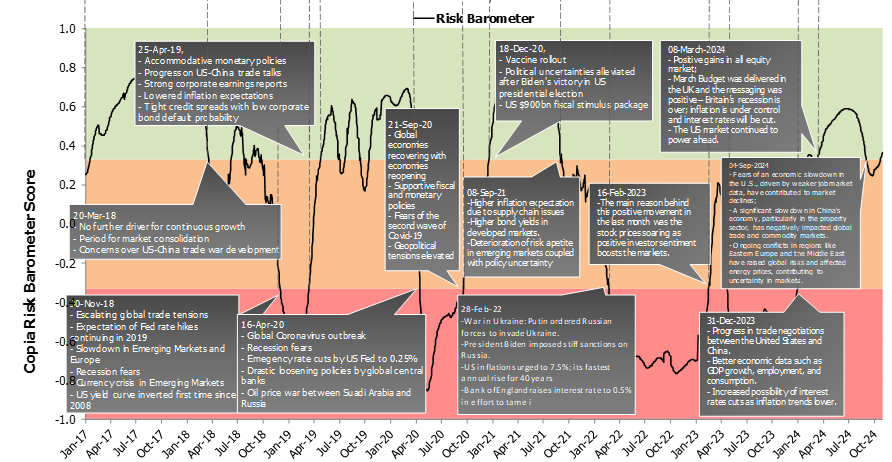

Market Pulse

Coming Up

- US FOMC Meeting Minutes, Tuesday 26th November 2024 at 7:00pm

- US CORE PCE Price Index data, Wednesday 27th November 2024 at 1:30pm (MoM) and 3:00pm (YoY)

- US GDP, Wednesday 27th November 2024 at 1:30pm

- CNY Manufacturing PMI, Saturday 30th November at 1:30am

Notice:

For professional advisers only, Copia does not provide financial advice, and the contents of this document should not be taken as such. The performance of each asset class is represented by certain Exchange Traded Funds available to UK investors and expressed in GBP terms selected by Copia Capital Management to represent that asset class, as reported at previous Thursday 4:30pm UK close. Reference to a particular asset class does not represent a recommendation to seek exposure to that asset class. This information is included for comparison purposes for the period stated, but is not an indicator of potential maximum loss for other periods or in the future.Open document settingsOpen publish panel