The infoshot to help kick-start your week

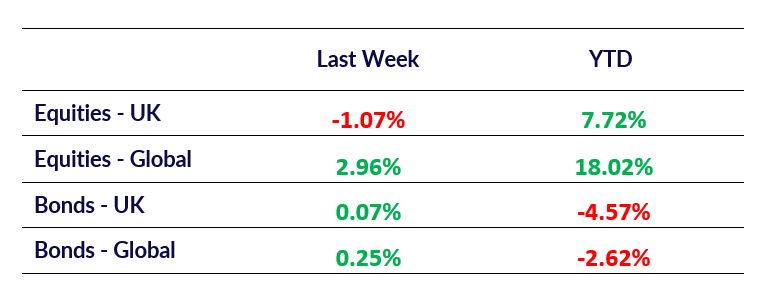

Last Week

- Donald Trump has reclaimed the U.S. presidency, marking a historic return to power eight years after his initial win over Hillary Clinton and four years after Joe Biden’s victory. Sweeping key battleground states, Trump secured what he called an “unprecedented and powerful mandate,” signalling a resurgence of the conservative populism he championed in 2016. With the Senate back in Republican hands, his administration faces a smoother path to confirm appointments and enact policies, from broad protective tariffs on imports to restructuring the federal government by appointing loyalists to key bureaucratic roles. Among his priorities, Trump has pledged significant tax incentives to boost domestic industries and to undertake an expansive deportation effort targeting undocumented immigrants. His foreign policy agenda includes promises to end the wars in Ukraine and Gaza, with a renewed “America first” focus. Assembling a coalition of influential allies such as Elon Musk, vaccine sceptic Robert F. Kennedy Jr., and former Democrat Tulsi Gabbard, Trump is set to reconfigure the political landscape, bringing a diverse array of supporters to shape his administration’s agenda as he prepares to take office in January.

- UK interest rates may fall more gradually after the Bank of England indicated inflation is expected to rise, following recent Budget measures. Although rates were reduced from 5% to 4.75%, the Bank highlighted that policies like lifting the cap on bus fares and applying VAT to private school fees could drive inflation higher. Bank Governor Andrew Bailey reiterated that while the direction is “downward,” cuts will be “gradual,” stressing global and domestic risks. Investors anticipate rates remaining steady for the rest of the year, with the next potential adjustment in early 2026. While inflation briefly fell below the 2% target in September, it’s projected to increase before easing back to 2% by 2027. The Bank’s Monetary Policy Committee voted 8-1 for the rate cut, with Catherine Mann dissenting, citing inflationary concerns tied to Budget impacts.

- The world remains off track to limit global temperature rise to 1.5°C above pre-industrial levels, though progress has been made, according to the International Energy Agency (IEA) in its World Energy Outlook 2024. Fossil fuels still comprise about 80% of the energy mix, down slightly from 82% a decade ago, even as energy demand has grown by 15%, with 40% of this increase met by clean energy. However, this shift is slow, as demand for fossil fuels has continued. Under current policies, fossil fuels will still contribute over half of global energy by 2050. While the “announced pledges” scenario (APS) projects a 1.7°C temperature increase, achieving the critical 1.5°C limit requires a rapid transition to a “net zero emissions by 2050” pathway. COP29, hosted in Baku this month, aims to address ways to accelerate these changes.

Market Pulse

Coming Up

- UK Average Earnings Index, Tuesday 12th November 2024 at 7:00am

- US Initial Jobless Claims, Thursday 14th November 2024 at 1:30am

- US Fed Chair Powell Speech, Thursday 14th November 2024 at 8:00pm

- UK GDP Data, Friday 15th November 2024 at 7:00am

Notice:

For professional advisers only, Copia does not provide financial advice, and the contents of this document should not be taken as such. The performance of each asset class is represented by certain Exchange Traded Funds available to UK investors and expressed in GBP terms selected by Copia Capital Management to represent that asset class, as reported at previous Thursday 4:30pm UK close. Reference to a particular asset class does not represent a recommendation to seek exposure to that asset class. This information is included for comparison purposes for the period stated, but is not an indicator of potential maximum loss for other periods or in the future.Open document settingsOpen publish panel