The infoshot to help kick-start your week

Last Week

- In Labour’s first Budget in 14 years, Chancellor Rachel Reeves introduced £40 billion in tax increases aimed at restoring economic stability and addressing a £22 billion fiscal gap. Key changes include a £25 billion hike in employer National Insurance contributions and increased rates for capital gains, inheritance, air passenger, and alcohol duties, while fuel duty will remain unchanged. Reeves also announced a 6.7% rise in the National Living Wage to £12.21, benefitting full-time workers. Additional funds include a £22 billion boost for the NHS, substantial defence funding, and enhanced support for education and local services. To support infrastructure, Reeves introduced new debt rules, allowing increased investment. Labour’s plan includes a phased elimination of the non-dom tax regime to enhance tax equity. Reeves pledged to stabilize the economy while addressing inflation, growth, and long-term fiscal health.

- Kemi Badenoch has been elected leader of the Conservative Party, receiving 53,806 votes to opponent Robert Jenrick’s 41,388. Badenoch, the North West Essex MP, expressed gratitude to her opponents and emphasized unity, pledging to restore standards within the party. She criticized past Conservative governments, calling for honesty and a “new start” to prepare for the next election. Badenoch’s campaign, Renewal 2030, aims to reclaim government control by addressing issues like national integrity and core values. Labour leaders, including Prime Minister Keir Starmer, extended congratulations, with some criticism highlighting Conservative party divisions. Badenoch previously served as shadow business and trade secretary and is known for her direct approach on sensitive topics, gaining popularity with party members.

- Over in the US, markets experienced volatility late in the week as concerns emerged around the growth prospects of technology and AI stocks, leading to declines in major indexes. The S&P 500 and NASDAQ posted weekly drops exceeding 1%, while the Dow’s dip was marginal. Despite market turbulence, the U.S. economy demonstrated resilience, with third-quarter GDP expanding at an annual rate of 2.8%, slightly below the previous quarter’s 3.0% but significantly higher than the first quarter’s 1.6%. Strong economic performance persisted despite inflation and high interest rates, providing a steady backdrop amid fluctuating market sentiment.

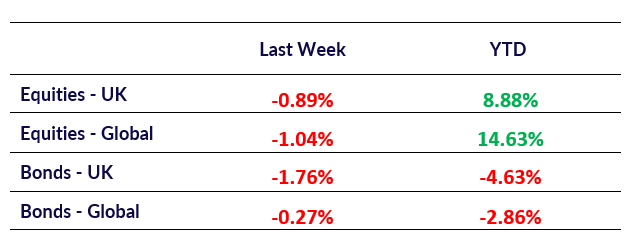

Market Pulse

Coming Up

- UK PMI Data, Tuesday 5th November 2024 at 9:30am

- US Presidential Election, Tuesday 5th November 2024 at 10:00am

- UK BoE Interest Rate Decision, Thursday 7th November 2024 at 12:00pm

- US Fed Interest Rate Decision, Thursday 7th November 2024 at 6:00pm

Notice:

For professional advisers only, Copia does not provide financial advice, and the contents of this document should not be taken as such. The performance of each asset class is represented by certain Exchange Traded Funds available to UK investors and expressed in GBP terms selected by Copia Capital Management to represent that asset class, as reported at previous Thursday 4:30pm UK close. Reference to a particular asset class does not represent a recommendation to seek exposure to that asset class. This information is included for comparison purposes for the period stated, but is not an indicator of potential maximum loss for other periods or in the future.Open document settingsOpen publish panel