The infoshot to help kick-start your week

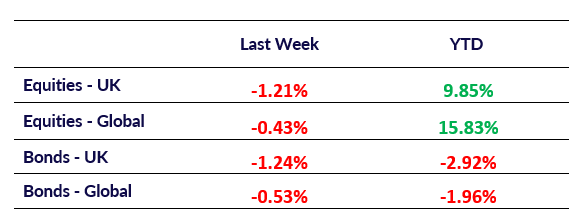

Last Week

- Asia-Pacific markets rose on Monday, with Japan leading gains following the country’s recent general election. Japan’s Nikkei 225 index climbed 1.8% as a weaker yen, which fell to a three-month low against the dollar, supported market sentiment. This currency shift followed Japan’s ruling Liberal Democratic Party’s loss of its majority in the lower house, adding potential near-term volatility to the USD-JPY exchange rate, according to TickMill’s Patrick Munnelly. Mainland China stocks also recovered from early declines, while Hong Kong’s benchmark index posted modest gains as investors looked to upcoming domestic and international developments. China’s top legislative body is set to meet from November 4-8, although the agenda does not include anticipated fiscal and debt policy discussions.

- The UK government’s debt is projected to rise to potentially unsustainable levels, according to official data, even as Chancellor Rachel Reeves introduces new fiscal guidelines. The revised methodology for calculating public debt will allow for £50 billion in borrowing while maintaining claims of balanced public finances. This change has sparked concerns about future financial liabilities for UK citizens, according to The Financial Mail on Sunday. Additionally, anticipated changes to inheritance tax in the upcoming budget have affected the stock market. Reports suggest that Reeves may remove the inheritance tax exemption for shares held over two years, leading to a significant sell-off and an 11.5% drop in the AIM index as investors adjust their portfolios. Education Secretary Bridget Phillipson has stated that Labour’s tax adjustments will not affect employees’ take-home pay. However, Reeves is expected to announce an increase in employers’ national insurance contributions, potentially generating between £8.5 billion and £20 billion in revenue, as reported by The Guardian.

- Brent Crude prices edged higher last week, approaching $75 a barrel, as the ongoing Middle East crisis remained a key focus for markets. Oil markets are sensitive to the risk of potential supply disruptions amid escalating tensions and whilst negotiations for a ceasefire and hostage releases are set to continue, recent intensified actions in the region have kept supply concerns elevated. However, despite these upward pressures, global demand is expected to soften due to economic slowdowns in the Eurozone and ongoing economic challenges in China, which are likely to weigh on longer-term demand expectations for oil.

Market Pulse

Coming Up

- US CB Consumer Confidence, Tuesday 29th October 2024 at 2:00pm

- US GDP Data, Wednesday 30th October 2024 at 12:30pm

- JPY BoJ Interest Rate Decision, Thursday 31st October 2024 at 3:00am

- US Employment Data, Friday 1st November 2024 at 12:30pm

Notice:

For professional advisers only, Copia does not provide financial advice, and the contents of this document should not be taken as such. The performance of each asset class is represented by certain Exchange Traded Funds available to UK investors and expressed in GBP terms selected by Copia Capital Management to represent that asset class, as reported at previous Thursday 4:30pm UK close. Reference to a particular asset class does not represent a recommendation to seek exposure to that asset class. This information is included for comparison purposes for the period stated, but is not an indicator of potential maximum loss for other periods or in the future.Open document settingsOpen publish panel