The infoshot to help kick-start your week

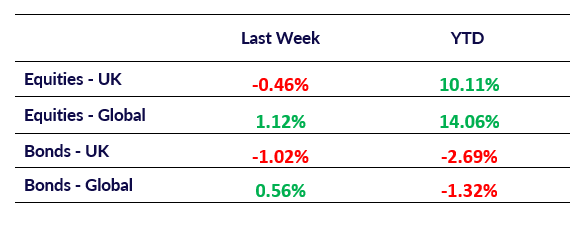

Last Week

- Asian stocks advanced on Monday, buoyed by stronger-than-expected US payroll data that underscored the resilience of the world’s largest economy. On Friday, both the S&P 500 and US Treasury yields rose as traders adjusted their outlooks, scaling back expectations of imminent Federal Reserve rate cuts. European equity futures posted modest gains today, while US futures remained relatively unchanged. Attention now turns to Tuesday, when mainland Chinese markets reopen after a week-long holiday. In the meantime, Goldman Sachs has upgraded its outlook on Chinese stocks to overweight, joining other analysts optimistic about the potential benefits of Beijing’s recent stimulus efforts. However, despite the optimism surrounding China’s economic recovery, some investors remain cautious. Firms such as Invesco, JPMorgan Asset Management, HSBC Global Private Banking and Wealth, and Nomura Holdings have expressed reservations, awaiting more concrete evidence that Beijing will deliver on its stimulus pledges. There are also concerns that certain stocks may already be approaching overvalued levels.

- Oil prices paused on Friday after experiencing their largest one-day surge in almost a year. Despite this, crude futures remain on track for a weekly gain, driven by concerns that Israel may target Iranian oil facilities in retaliation for a missile attack earlier in the week. Traders are wary that such a move could provoke a wider conflict, potentially disrupting global energy supplies. Meanwhile, Israel reported striking more than a dozen Hezbollah targets in Beirut on Thursday. In other markets, gold edged higher on Friday, while the US dollar remained largely unchanged.

- French Prime Minister Michel Barnier confirmed that planned tax increases aimed at addressing the country’s budget deficit will affect approximately 300 of France’s largest companies. Speaking on France 2 television, Barnier stated that the tax hikes will be temporary, lasting one to two years, and will apply to companies with annual revenues of €1 billion or more. These comments add further detail to the government’s broader plan, announced earlier this week, which includes around €60 billion in spending cuts and tax increases. The measures are aimed at narrowing the budget deficit and reinforcing investor confidence. The 2025 budget proposal will be presented to the cabinet and parliament on October 10 for debate and potential revisions.

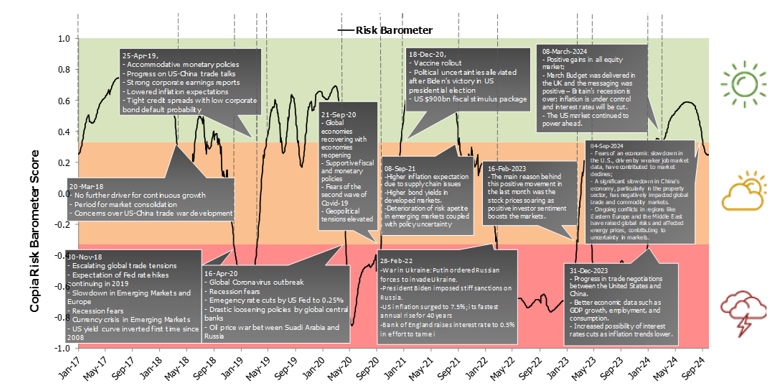

Market Pulse

Coming Up

- US FOMC Meeting Minutes, Wednesday 9th October 2024 at 7:00pm

- US CPI Data, Thursday 10th October 2024 at 1:30pm

- UK GDP Data, Friday 11th October 2024 at 7:00am

Notice:

For professional advisers only, Copia does not provide financial advice, and the contents of this document should not be taken as such. The performance of each asset class is represented by certain Exchange Traded Funds available to UK investors and expressed in GBP terms selected by Copia Capital Management to represent that asset class, as reported at previous Thursday 4:30pm UK close. Reference to a particular asset class does not represent a recommendation to seek exposure to that asset class. This information is included for comparison purposes for the period stated, but is not an indicator of potential maximum loss for other periods or in the future.Open document settingsOpen publish panel