The infoshot to help kick-start your week

Last Week

- The Federal Reserve is poised to make a significant policy shift this week by lowering interest rates for the first time in over four years, as it aims to engineer a rare soft landing for the U.S. economy. With inflation appearing to be under control and signs of weakness emerging in the labour market, the Fed is widely expected to reduce its benchmark lending rate by at least a quarter percentage point at the conclusion of its two-day meeting on Wednesday. In the UK, the Bank of England is expected to maintain a cautious approach to rate cuts, despite increasing calls from some investors for more aggressive easing measures. Meanwhile, in Europe, the European Central Bank (ECB) may continue to ease policy but must carefully monitor consumer-price growth, according to Governing Council member Pierre Wunsch.

- The U.S. stock market has regained most of the losses incurred during its summer selloff, but this recovery stands out as it is not driven by Big Tech. While the S&P 500 has rebounded in the past, this time the leadership has shifted away from technology giants like Nvidia Corp. and Microsoft Corp., which had fuelled market gains over the past two years with their strong profits and exposure to artificial intelligence. Instead, investors are rotating into traditionally defensive sectors such as real estate, utilities, and consumer staples. This shift comes as the Federal Reserve’s anticipated move toward interest rate cuts raises concerns about slowing economic growth. Since the S&P 500’s peak on July 16, technology stocks have largely declined, with the Bloomberg Magnificent 7 Index down 5.3%. Meanwhile, real estate and utilities have surged, both posting gains of 11%.

- Asking prices for UK homes rose at double their long-term average pace in September, reflecting renewed confidence among sellers following the Bank of England’s first interest rate cut in over four years. According to a report from property site Rightmove, the average price of homes listed on the market increased by 0.8%, reaching £370,759 ($487,000). While price hikes in September are typical, the size of this increase suggests that lower borrowing costs and a rise in available properties are helping to unlock pent-up demand from the past year. This optimism has also resulted in a surge in supply, with the average number of properties per estate agent reaching its highest level since 2014. Additionally, the number of agreed sales has increased by more than 25% compared to 2023 levels.

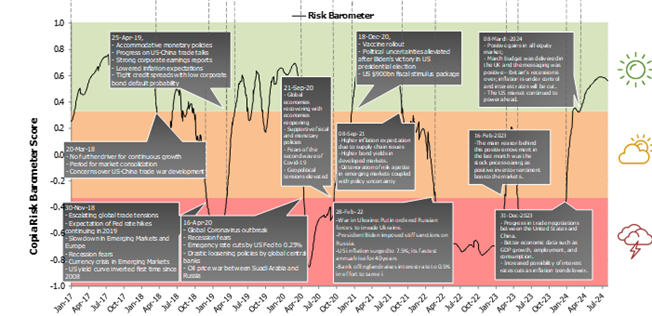

Market Pulse

Coming Up

- UK CPI Data, Wednesday 18th September 2024 at 7:00am

- EUR CPI Data, Wednesday 18th September 2024 at 10:00am

- US Fed Interest Rate Decision, Wednesday 18th September 2024 at 12:00pm

- UK BoE Interest Rate Decision, Thursday 19th September 2024 at 12:00pm

Notice:

For professional advisers only, Copia does not provide financial advice, and the contents of this document should not be taken as such. The performance of each asset class is represented by certain Exchange Traded Funds available to UK investors and expressed in GBP terms selected by Copia Capital Management to represent that asset class, as reported at previous Thursday 4:30pm UK close. Reference to a particular asset class does not represent a recommendation to seek exposure to that asset class. This information is included for comparison purposes for the period stated, but is not an indicator of potential maximum loss for other periods or in the future.Open document settingsOpen publish panel