The infoshot to help kick-start your week

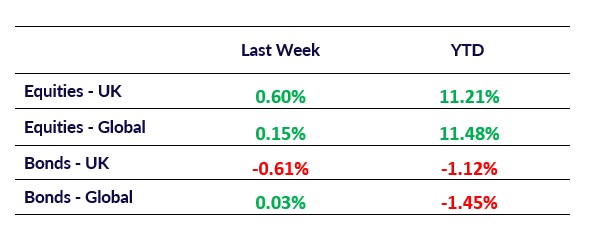

Last Week

- The recent optimism surrounding the potential for European equities to outperform their U.S. counterparts appears to be waning, as concerns about an economic slowdown have started to weigh on European earnings forecasts. While Europe initially seemed poised to benefit from a rotation away from large-cap technology stocks, investors are increasingly favouring undervalued sectors within the U.S. market. This shift in preference is largely driven by data indicating the resilience of the U.S. economy, coupled with growing expectations that the Federal Reserve may implement interest rate cuts sooner and more aggressively than previously projected. Although the European market remains strong, as evidenced by the Stoxx 600 reaching record levels, the index underperformed the S&P 500 in August. On a year-to-date basis, the Stoxx 600 has also lagged behind the S&P 500 by nearly 9 percentage points, marking the second consecutive year of relative underperformance.

- Top-performing emerging-market bond managers are adjusting their portfolios in response to the potential for a significant U.S. interest rate cut, which could provide renewed support to an asset class that has experienced nearly $15 billion in outflows this year. Leading investment firms, including Pacific Investment Management Co., Neuberger Berman, and Grantham Mayo Van Otterloo & Co., are increasingly focused on local-currency debt and specific reform-driven opportunities in countries such as Ecuador and Argentina. These markets are expected to benefit the most from the positive impact that Federal Reserve rate cuts could have on risk assets. However, emerging markets remain subject to volatility due to ongoing global economic uncertainty and regional conflicts, which continue to challenge optimistic forecasts.

- Investors are closely monitoring the situation in Germany, where Chancellor Olaf Scholz’s ruling coalition faced significant setbacks in two regional elections held on Sunday. Populist parties from both the extreme right and left secured over 60% of the vote in Thuringia and nearly half in Saxony. Despite these developments, the immediate market impact is expected to be minimal, especially given that Germany’s benchmark DAX equity index reached a record high last week. However, the rise of the Alternative for Germany (AfD) party is notable, as it is projected to win 32.8% of the vote in Thuringia, marking the first victory for a far-right party in a German state election since World War II. While the AfD is unlikely to form a government due to its exclusion by other parliamentary parties, its success could have longer-term implications for the political landscape.

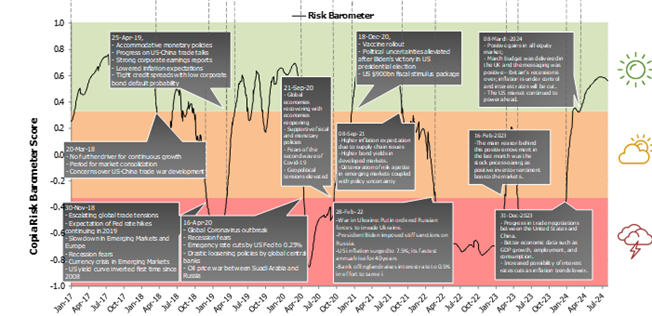

Market Pulse

Coming Up

- US Manufacturing PMI, Tuesday 3rd September 2024 at 2:45pm

- UK Composite and Services PMI, Wednesday 4th September 2024 at 9:30am

- UK Halifax House Price Index, Friday 6th September 2024 at 7:00am

- US Unemployment Rate, Friday 6th September 2024 at 1:30pm

Notice:

For professional advisers only, Copia does not provide financial advice, and the contents of this document should not be taken as such. The performance of each asset class is represented by certain Exchange Traded Funds available to UK investors and expressed in GBP terms selected by Copia Capital Management to represent that asset class, as reported at previous Thursday 4:30pm UK close. Reference to a particular asset class does not represent a recommendation to seek exposure to that asset class. This information is included for comparison purposes for the period stated, but is not an indicator of potential maximum loss for other periods or in the future.Open document settingsOpen publish panel