The infoshot to help kick-start your week

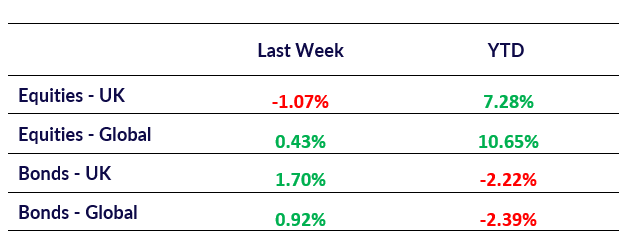

Last Week

- The French bond market experienced increased volatility due to political uncertainty. French securities declined on Thursday amid concerns that Marine Le Pen’s National Rally party might implement looser fiscal policies if it wins the upcoming elections. This has caused a significant rise in the spread between French and German debt yields, reaching levels not seen since the European debt crisis in 2011. As of early today, French bond futures remain largely steady. Meanwhile, G-7 leaders have expressed concerns over President Macron’s strategic decision to hold a snap election.

- With less than three weeks remaining before the UK general election, Prime Minister Rishi Sunak is contending with unfavourable polls that indicate a slim chance of reversing his Conservative Party’s decline before the July 4 vote. Following the release of election manifestos by Britain’s two main parties last week, Keir Starmer’s Labour opposition has widened its lead in polls conducted by the Observer and the Sunday Telegraph. A seat-by-seat analysis by Survation predicts Labour will secure a large majority, while the Conservatives are projected to win just 72 out of 650 seats in the House of Commons, a steep drop from the 365 seats won in the 2019 election. Additionally, Nigel Farage’s Reform UK is forecasted to win seven seats. Financial issues, particularly concerns over national debt and spending promises.

- China reported mixed economic data, with industrial expansion slowing in May while retail spending exceeded forecasts, suggesting some easing of deep imbalances in the economic recovery. According to the National Bureau of Statistics, industrial production rose 5.6% year-on-year, down from April’s 6.7% increase and below the median forecast of 6.2% from a Bloomberg survey. Retail sales, on the other hand, accelerated, rising 3.7% compared to a forecast of 3%. These spending figures indicate that Chinese households might be starting to respond to government efforts to boost consumption. However, home prices fell more sharply in May, with new-home prices, excluding state-subsidized housing, decreasing in 70 cities. Additionally, the People’s Bank of China maintained a key interest rate unchanged for the tenth consecutive month just before the data release.

Market Pulse

Coming Up

- UK BoE Interest Rate Decision, Thursday 20th June 2024 at 12:00 pm

- UK BoE Inflation Letter, Thursday 20th June 2024 at 1:00 pm.

- UK PMI Data, Friday 21st June 2024 at 9:30am

- US Fed Monetary Policy Report, Friday 21st June at 4:00 pm.

Notice:

For professional advisers only, Copia does not provide financial advice, and the contents of this document should not be taken as such. The performance of each asset class is represented by certain Exchange Traded Funds available to UK investors and expressed in GBP terms selected by Copia Capital Management to represent that asset class, as reported at previous Thursday 4:30pm UK close. Reference to a particular asset class does not represent a recommendation to seek exposure to that asset class. This information is included for comparison purposes for the period stated, but is not an indicator of potential maximum loss for other periods or in the future.Open document settingsOpen publish panel