The infoshot to help kick-start your week

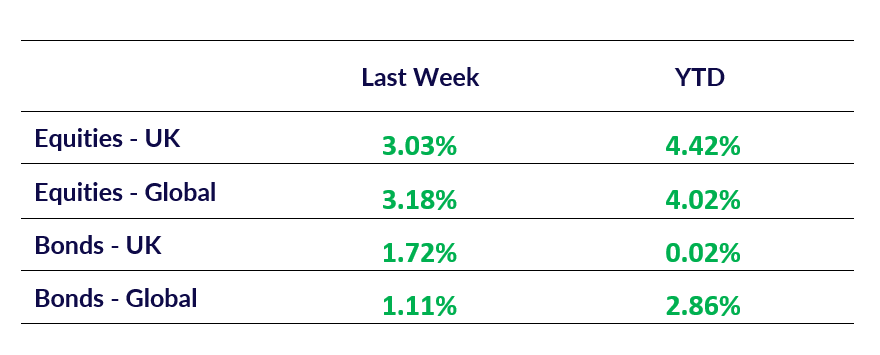

Last Week

- Traders in the swaps market have significantly increased their bets on an interest rate hike by the Bank of Japan (BOJ) at its upcoming 23-24 January meeting, with the likelihood rising to nearly 99% from 71% earlier in the week. Market expectations were bolstered by BOJ Governor Kazuo Ueda’s comments on Wednesday, suggesting a decision on rates would be made soon and expressing confidence in wage growth. Japan’s government bond yields have climbed, with the 2-year yield reaching its highest level since 2008. The yen strengthened to 154.98 against the dollar on Friday, marking its strongest level since December. Finance Minister Katsunobu Kato reiterated the BOJ’s independence in pursuing price stability but acknowledged the natural link between rising wages, prices, and interest rates. Nearly three-quarters of economists now predict a hike, with policymakers adopting a transparent approach to reduce market volatility ahead of the decision.

- TikTok has resumed operations in the US following President-elect Donald Trump’s pledge to reinstate the app’s access. Speaking at a rally on Sunday, Trump stressed the importance of preserving the platform, which is used by 170 million Americans, and suggested a joint venture to secure its future. In a statement, TikTok thanked Trump for providing clarity that service providers would not face penalties, enabling the app to support over 7 million small businesses. The platform had been removed from US app stores after a ban citing national security concerns. Trump intends to delay the ban’s enforcement to negotiate a deal that safeguards US interests, potentially involving 50% American ownership in a joint venture. This development occurs amidst strained US-China relations, with China calling for fair business practices. TikTok’s restoration reflects a shift from Trump’s earlier stance, acknowledging the app’s economic value and influence among younger users.

- The S&P 500 posted its strongest weekly performance since the November presidential election, rising 2.9% ahead of Donald Trump’s inauguration. On Friday, the index gained 1%, with Nvidia, Tesla, and Intel leading the charge. Intel surged over 9% on reports of a potential acquisition. Market sentiment was further lifted by news that Trump and Chinese President Xi Jinping discussed trade, TikTok, and fentanyl, signalling a possible framework for future relations between the two economic powers. Bond markets also rebounded, with 10-year Treasury yields falling by 15 basis points over the week. Cooling inflation data and strong earnings reports from financial companies contributed to a rally in both stocks and bonds. Analysts highlighted that easing inflation and stabilising sentiment among investors are supporting market recovery. The Nasdaq 100 rose 1.7%, while the Dow Jones added 0.8%. Markets will be closed on Monday for a public holiday, with investors watching earnings season closely for further direction.

Market Pulse

Coming Up

- UK Average Earnings Index +Bonus, Tuesday 21st January 2025 at 7:00am

- US Initial Jobless Claims, Thursday 23rd January 2025 at 1:30pm

- BoJ Interest Rate Decision, Friday 24th January 2025 at 3:00am

Notice:

For professional advisers only, Copia does not provide financial advice, and the contents of this document should not be taken as such. The performance of each asset class is represented by certain Exchange Traded Funds available to UK investors and expressed in GBP terms selected by Copia Capital Management to represent that asset class, as reported at previous Thursday 4:30pm UK close. Reference to a particular asset class does not represent a recommendation to seek exposure to that asset class. This information is included for comparison purposes for the period stated, but is not an indicator of potential maximum loss for other periods or in the future.Open document settingsOpen publish panel