The infoshot to help kick-start your week

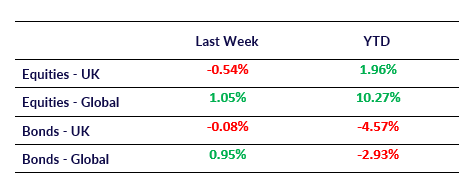

Last Week

- UK inflation slowed more than expected to 4.6 per cent in October as a result of lower energy prices. The rate was lower than the 6.7 per cent seen in September and below the 4.8 per cent predicted by economists. The core CPI rate, which excludes volatile food and energy, was down to 5.7 per cent in October from 6.1 per cent the month before.

- US inflation fell more than expected to 3.2 per cent in October which stimulate a rally in stock and bond markets. Inflation is down from the 3.7 per cent figure seen in September and sat slightly below economist’s expectations of 3.3 per cent. The S&P 500 jumped 1.9 per cent on Tuesday as a result of the news and maintained this level throughout the week.

- Brent crude fell 4.6 per cent on Thursday as it hit its lowest level since July. While the price of Brent crude has recovered since, there is pressure on members of Opec+ ahead of its upcoming meeting on the 26th of November with oil prices falling over the last two months on the back of slowing global growth.

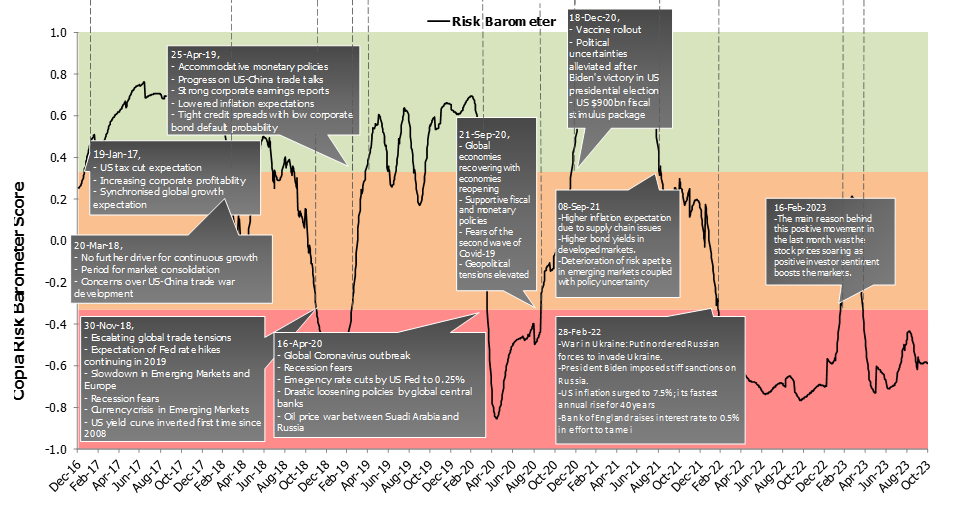

Market Pulse

Coming Up

- US October Existing Home Sales data released, 21st November at 3:00pm.

- US Initial Jobless Claims data released, 22nd November at 1:30pm.

- UK PMI data released, 23rd November at 9:30am.

Notice:

For professional advisers only, Copia does not provide financial advice, and the contents of this document should not be taken as such. The performance of each asset class is represented by certain Exchange Traded Funds available to UK investors and expressed in GBP terms selected by Copia Capital Management to represent that asset class, as reported at previous Thursday 4:30pm UK close. Reference to a particular asset class does not represent a recommendation to seek exposure to that asset class. This information is included for comparison purposes for the period stated, but is not an indicator of potential maximum loss for other periods or in the future.Open document settingsOpen publish panel