The infoshot to help kick-start your week

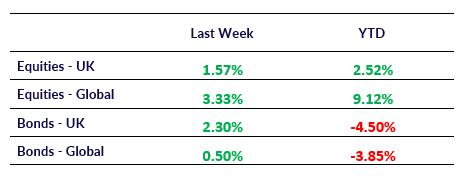

Last Week

- Eurozone inflation reached its lowest point in more than two years as it fell to 2.9 per cent in October. The figure was down from 4.3 per cent in September and undershot expectations of 3.1 per cent. The data comes after the ECB decided to hold interest rates steady at 4 per cent the week before as the central banks tries to get a balance between controlling inflation without pushing the bloc into a sharp recession.

- The Bank of England kept rates steady at 5.25% but warned that the high rate will remain for a reasonable period as the UK central bank aims to bring down persistent inflation in the country. The news came shortly after the US Federal Reserve also hold interest rates at their 22-year high after a month of strong economic data suggested that it is far too soon to consider rate cuts.

- US stocks rallied after a slowdown in hirings was announced towards the end of last week. It was reported that 150,000 new jobs were created in October compared to the 297,000 created in September. The data also comes under analyst estimates of 180,000 new jobs and analysts are suggesting that higher interest rates could be taking effect on the stubbornly strong labour market.

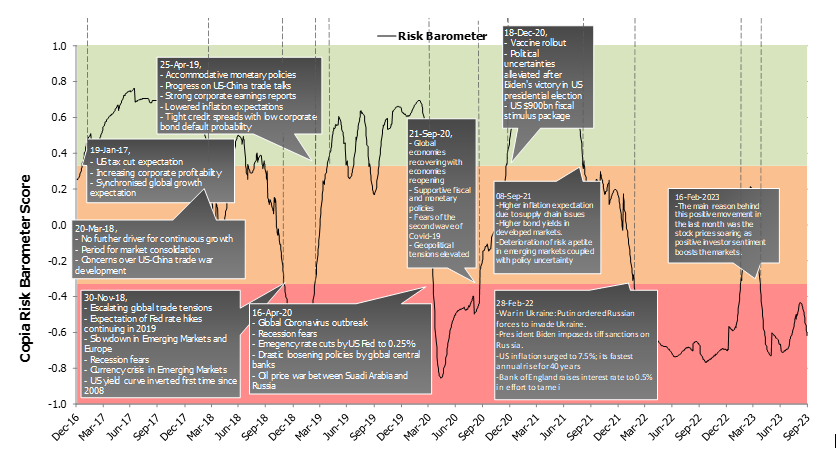

Market Pulse

Coming Up

- US Initial Jobless Claims data released, November 9th at 2:30pm.

- UK Q3 GDP data released, November 10th at 8:00am.

Notice:

The performance of each asset class is represented by certain Exchange Traded Funds available to UK investors and expressed in GBP terms selected by Copia Capital Management to represent that asset class, as reported at previous Thursday 4:30pm UK close. Reference to a particular asset class does not represent a recommendation to seek exposure to that asset class. This information is included for comparison purposes for the period stated, but is not an indicator of potential maximum loss for other periods or in the future.Open document settingsOpen publish panel