The infoshot to help kick-start your week

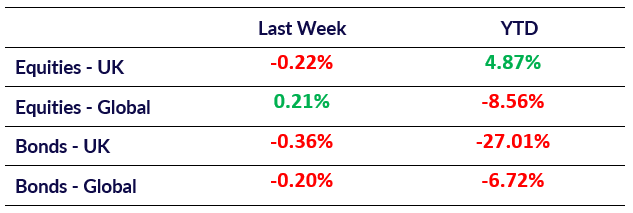

Last Week

The major US averages closed 2022 with the worst annual losses since 2008. while UK markets have enjoyed better luck than their peers. The Dow Jones ended the year down about 8.8%, the S&P 500 lost 19.4% and the tech-heavy Nasdaq tumbled 33.1% last year. While the UK’s FTSE 100 fared better than its peers, the more domestically-oriented FTSE 250 dropped 19.7% this year.

The British Retail Consortium forecast a particularly difficult 6 months ahead, as consumers try to cope with higher prices by buying less. 2022 was a difficult year for retailers, as just over 17000 shops shut across the UK’s high streets. Moving into 2023, the BRC predicts sales will grow 2.3% at most in the first half of the year. Furthermore, there remains the issue of rising costs for retailers, and the end of the government’s support for firms’ energy bills is fast approaching.

The UK becomes the latest country to require negative covid tests for China arrivals as cases surge following Beijing’s decision to relax its zero-Covid policy. While Asian shares ended 2022 positively, uncertainty over the Covid data and the introduction of new arrival restrictions curb optimism around Beijing’s unlock. The added uncertainty will weigh on markets going into 2023.

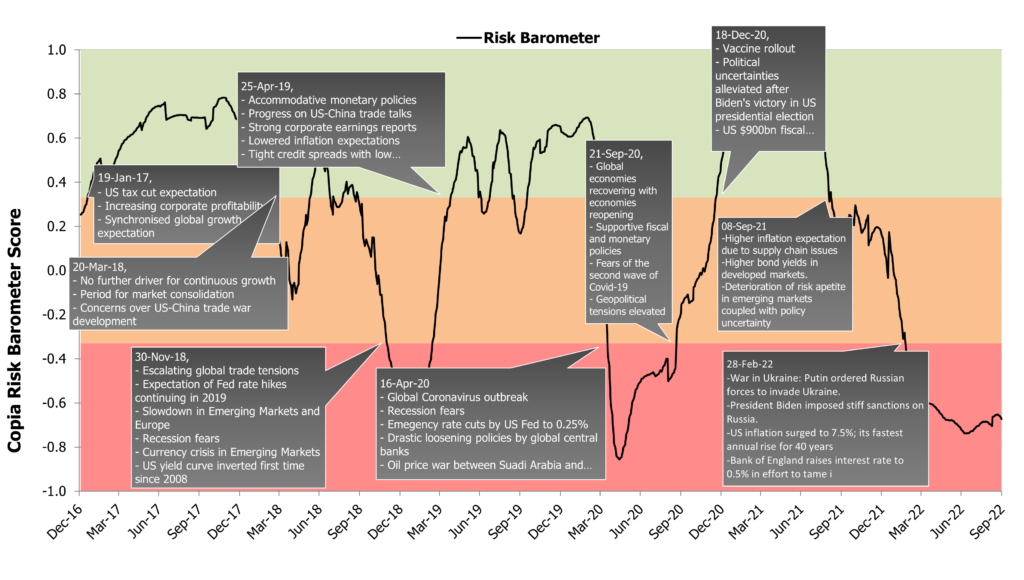

Market Pulse

Coming Up

- FOMC Meeting Minutes released 4th January

- EU CPI (YoY Dec) released 6th January, forecasted at 9.7%

Notice:

The performance of each asset class is represented by certain Exchange Traded Funds available to UK investors and expressed in GBP terms selected by Copia Capital Management to represent that asset class, as reported at previous Thursday 4:30pm UK close. Reference to a particular asset class does not represent a recommendation to seek exposure to that asset class. This information is included for comparison purposes for the period stated, but is not an indicator of potential maximum loss for other periods or in the future.Open document settingsOpen publish panel