Pete Wasko, Senior Portfolio Manager, Copia Capital

It was a surprise to many that President Donald Trump authorised Operation Midnight Hammer just six months into his term, particularly given that he was elected on an anti-war ticket.

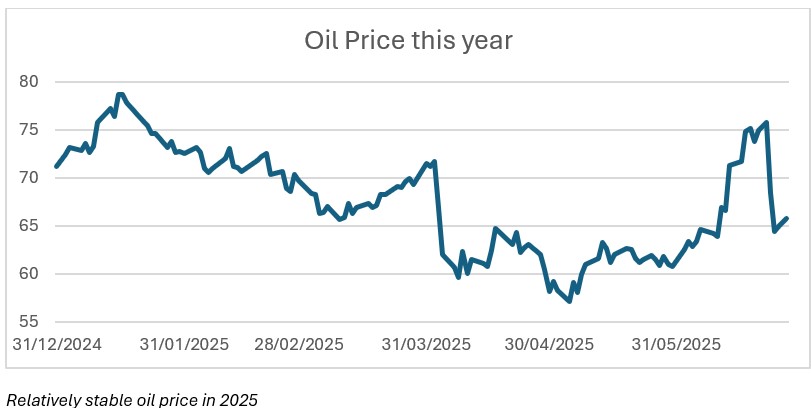

Although there were some fluctuations in oil prices, they remained largely stable in comparison with prices earlier in the year. Investment markets also held steady, even following the US involvement.

The critical element is the unexpected indication that Trump may be more likely to engage militarily than previously thought. For investors, many may be wondering what might happen in the markets if a larger conflict were to happen in the future. With that in mind, I thought it would be helpful explore the factors at play and how different scenarios could impact investments.

US intervention

I’m not going to dwell too long on what intricate political manoeuvres may have led to the US authorising strikes on Iran’s nuclear facilities. Nonetheless, given that American intervention represents a key factor in how markets might react, it’s important to go over a few of the dynamics in this instance.

Trump’s primary motive was to disrupt Iran’s nuclear programme. He has historically been an Iran hawk, having taken America out of a nuclear agreement with Tehran and ordered the assassination of Qasem Soleimani, Iran’s most powerful general, during his first term.

The bombings of the facilities appear, in part, to fulfil Trump’s long-term ambition to defang Iran’s nuclear ambitions. What was seen as a telegraphed response when Iran directed missiles at a US base in Qatar would indicate a reticence to escalate further.

An interesting aspect of the decision is it doesn’t split neatly along Republican and Democrat party lines. Even within the MAGA movement, there was a pronounced divide between idealogues.

This indicates that further intervention may not have the MAGA support which Trump usually enjoys, potentially complicating US involvement in future conflicts.

What the market reaction tells us

Almost every asset class saw a muted response during the affair. Currencies, bonds, indices and commodities alike remained stable and were nowhere near the distress displayed during ‘Liberation Day’.

One crucial element was whether Iran would cut off the Strait of Hormuz, through which some 20% of the world’s oil travels. Some speculated this could push oil to $130 a barrel.

Tehran did give approval to do this, if necessary, but it would have been far more devastating for them economically than the more energy independent America. Also, it would have strained relations with China, which receives 13.6% of their Brent crude from Iran and could be a considerable blow to their growth. The oil markets seemed comfortable in the bet that this would not happen.

What other conflicts tell us

Russia’s invasion of Ukraine, which came at a time of inflationary stress following the pandemic, prompted a far more volatile market response. This was largely because Russia played a more active role in the global economy, particularly in energy and finance, than Iran does.

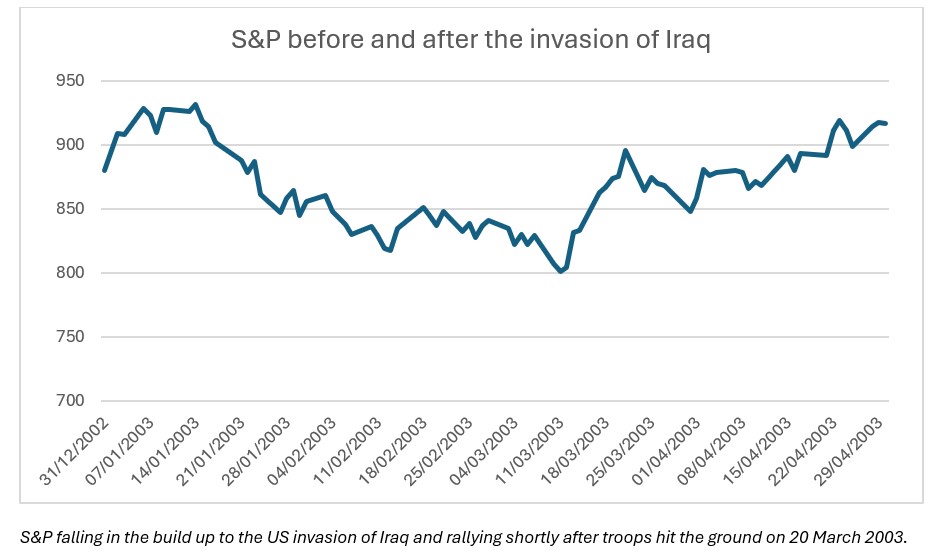

When we consider US interventionism, such as in Iraq, most of the market stress had occurred prior to boots hitting the ground. It is reductive, but markets dislike prolonged uncertainty. Once troops are deployed in foreign territory predicting an exit strategy or progress becomes largely impossible. Combined with any inflationary pressures, it can make it difficult for markets to form a clear trading strategy.

Best-case and worst-case scenarios

The markets’ muted response to Operation Midnight Hammer indicates that, although a surprise, intervention was restrained and Tehran had little room to manoeuvre. So far, it looks like the stated aim of the strikes, to disrupt Iran’s nuclear ambitions has been achieved, although there’s some contention over the extent.

The best case-scenario now would involve a cessation of hostilities between Iran and Israel, with the US stepping in to negotiate a new nuclear deal with Iran. This should keep oil tankers moving through Hormuz and reassure markets that the strikes were a one-off, with little chance of prolonged conflict.

The worst-case scenario would involve the ceasefire breaking down, Tehran shutting off the Strait, and the US putting boots on the ground. This would likely cause oil prices to rise and inflation to bite. A significant increase in defence spending would potentially push up borrowing and put more pressure on US Treasury yields. It will also create a lot of uncertainty which would diminish market confidence.

Don’t take your eye off the ball

While the risk of conflict may be higher than before, which should be factored into investment decisions, it’s important not to lose sight of other key events.

It has been suggested that one of the most consequential aspects of America’s involvement in the Iran conflict is that it makes trade deals to avoid looming tariff deadlines less likely. Markets appear to be learning, or perhaps fatiguing, from Trump’s unorthodoxy, with some taking the ‘TACO’ (Trump always chickens out) mindset.

It is important to be prepared for speculative or surprise outcomes like conflicts, but make sure you don’t also lose sight of the bigger picture.

This article is intended for regulated financial advisers and investment professionals only. Copia does not provide financial advice. This information is not intended as financial advice and should not be interpreted as such.

Free at 10am on Tuesday 15 July?

Join Tony Hicks and Pete Wasko for our second Quarterly Market Review of 2025. They’ll be covering an array of topics including what a prolonged conflict in the Middle East might mean for markets and your client’s investment. You can register here >

30th June 2025

Navigating conflict as an investor

Pete Wasko, Senior Portfolio Manager, Copia Capital

It was a surprise to many that President Donald Trump authorised Operation Midnight Hammer just six months into his term, particularly given that he was elected on an anti-war ticket.

Although there were some fluctuations in oil prices, they remained largely stable in comparison with prices earlier in the year. Investment markets also held steady, even following the US involvement.

The critical element is the unexpected indication that Trump may be more likely to engage militarily than previously thought. For investors, many may be wondering what might happen in the markets if a larger conflict were to happen in the future. With that in mind, I thought it would be helpful explore the factors at play and how different scenarios could impact investments.

US intervention

I’m not going to dwell too long on what intricate political manoeuvres may have led to the US authorising strikes on Iran’s nuclear facilities. Nonetheless, given that American intervention represents a key factor in how markets might react, it’s important to go over a few of the dynamics in this instance.

Trump’s primary motive was to disrupt Iran’s nuclear programme. He has historically been an Iran hawk, having taken America out of a nuclear agreement with Tehran and ordered the assassination of Qasem Soleimani, Iran’s most powerful general, during his first term.

The bombings of the facilities appear, in part, to fulfil Trump’s long-term ambition to defang Iran’s nuclear ambitions. What was seen as a telegraphed response when Iran directed missiles at a US base in Qatar would indicate a reticence to escalate further.

An interesting aspect of the decision is it doesn’t split neatly along Republican and Democrat party lines. Even within the MAGA movement, there was a pronounced divide between idealogues.

This indicates that further intervention may not have the MAGA support which Trump usually enjoys, potentially complicating US involvement in future conflicts.

What the market reaction tells us

Almost every asset class saw a muted response during the affair. Currencies, bonds, indices and commodities alike remained stable and were nowhere near the distress displayed during ‘Liberation Day’.

One crucial element was whether Iran would cut off the Strait of Hormuz, through which some 20% of the world’s oil travels. Some speculated this could push oil to $130 a barrel.

Tehran did give approval to do this, if necessary, but it would have been far more devastating for them economically than the more energy independent America. Also, it would have strained relations with China, which receives 13.6% of their Brent crude from Iran and could be a considerable blow to their growth. The oil markets seemed comfortable in the bet that this would not happen.

What other conflicts tell us

Russia’s invasion of Ukraine, which came at a time of inflationary stress following the pandemic, prompted a far more volatile market response. This was largely because Russia played a more active role in the global economy, particularly in energy and finance, than Iran does.

When we consider US interventionism, such as in Iraq, most of the market stress had occurred prior to boots hitting the ground. It is reductive, but markets dislike prolonged uncertainty. Once troops are deployed in foreign territory predicting an exit strategy or progress becomes largely impossible. Combined with any inflationary pressures, it can make it difficult for markets to form a clear trading strategy.

Best-case and worst-case scenarios

The markets’ muted response to Operation Midnight Hammer indicates that, although a surprise, intervention was restrained and Tehran had little room to manoeuvre. So far, it looks like the stated aim of the strikes, to disrupt Iran’s nuclear ambitions has been achieved, although there’s some contention over the extent.

The best case-scenario now would involve a cessation of hostilities between Iran and Israel, with the US stepping in to negotiate a new nuclear deal with Iran. This should keep oil tankers moving through Hormuz and reassure markets that the strikes were a one-off, with little chance of prolonged conflict.

The worst-case scenario would involve the ceasefire breaking down, Tehran shutting off the Strait, and the US putting boots on the ground. This would likely cause oil prices to rise and inflation to bite. A significant increase in defence spending would potentially push up borrowing and put more pressure on US Treasury yields. It will also create a lot of uncertainty which would diminish market confidence.

Don’t take your eye off the ball

While the risk of conflict may be higher than before, which should be factored into investment decisions, it’s important not to lose sight of other key events.

It has been suggested that one of the most consequential aspects of America’s involvement in the Iran conflict is that it makes trade deals to avoid looming tariff deadlines less likely. Markets appear to be learning, or perhaps fatiguing, from Trump’s unorthodoxy, with some taking the ‘TACO’ (Trump always chickens out) mindset.

It is important to be prepared for speculative or surprise outcomes like conflicts, but make sure you don’t also lose sight of the bigger picture.

This article is intended for regulated financial advisers and investment professionals only. Copia does not provide financial advice. This information is not intended as financial advice and should not be interpreted as such.

Free at 10am on Tuesday 15 July?

Join Tony Hicks and Pete Wasko for our second Quarterly Market Review of 2025. They’ll be covering an array of topics including what a prolonged conflict in the Middle East might mean for markets and your client’s investment. You can register here >