A relaxed read on the issues of the day

Occasionally, there are slow months when we feel we are reporting on more trifling matters. July was not one of those months. July was a month of significant volatility, driven by political and economic news.

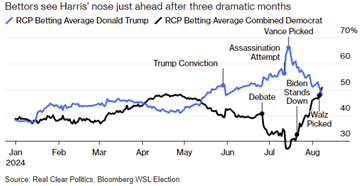

At the start of the month was the shooting at the Pennsylvania political rally, two lives were ended and a bloodied Donald Trump surged in popularity as many voters understandably sympathised with the candidate. US stock markets shifted markedly as investors looked to interpret the likely winners and losers from a Trump presidency. This event arguably accelerated the withdrawal of Joe Biden as the rival Democrat candidate, endorsing Kamala Harris, his VP, to replace him. The Democrats have been gaining ground in the weeks since.

The US economy has been resilient, and growth has been stronger than in many other countries, but markets were surprised by data suggesting the US labour market is weaker than expected and that growth may fade. Investors took this as a signal that interest rate cuts would follow and this helped bonds, property and smaller companies to perform, all of which are supported by falling interest rates.

In equity markets, companies have reported their earnings for the 3-month period to the end of June to investors. Among US companies, over half we’re doing better than expected, indicating a healthy economy, but there was concern over some of the very large businesses linked to the Artificial Intelligence investment theme. These businesses have seen their share prices appreciate rapidly over the last 18 months but despite enormous sums being invested in AI, it has not born fruit yet and revenues linked to AI have yet to come through.

UK companies did well. Economic growth has been stronger than expected and businesses are reporting that they have strong order books. The general election had little impact as The Labour Party were heavy favourites to win and the result was in line with this.

European markets posted a small gain however trailed the UK market on the back of uncertainty around French elections as well as some softer economic data points. Japanese stocks posted gains over the period although this was entirely attributed to a rally in the Yen. The Bank of Japan raised interest rates by 0.25% (the first increase since 2007), while other developed market Central Banks are poised to cut rates, this led the Yen appreciating nearly 5% against the Pound in July. Emerging Markets finished the month down as gains in India were more than offset by losses in China and Latin America.

In bond markets, investor optimism that weaker inflation in the US will lead to lower interest rates supported the performance of US government bonds. UK Gilts also performed well, but as interest rates are not expected fall as quickly in the UK, they did not quite match their US counterparts. Bonds issued by high quality businesses performed better than those of low-quality businesses.

In portfolios we continue to focus on diversification across regions to offer some protection from market volatility and to take advantage of cheaper valuations. Some of the market volatility around the end of the month may have been exacerbated by fewer buyers and sellers being active over the summer period, but we believe the fear of recession is overdone and US growth will continue to hold up, at least in the near term.

This information is intended for professional financial advisers only. Copia does not provide financial advice. This information is not intended as financial advice and should not be interpreted as such.

14th August 2024

Cappuccino Commentary

A relaxed read on the issues of the day

Occasionally, there are slow months when we feel we are reporting on more trifling matters. July was not one of those months. July was a month of significant volatility, driven by political and economic news.

At the start of the month was the shooting at the Pennsylvania political rally, two lives were ended and a bloodied Donald Trump surged in popularity as many voters understandably sympathised with the candidate. US stock markets shifted markedly as investors looked to interpret the likely winners and losers from a Trump presidency. This event arguably accelerated the withdrawal of Joe Biden as the rival Democrat candidate, endorsing Kamala Harris, his VP, to replace him. The Democrats have been gaining ground in the weeks since.

The US economy has been resilient, and growth has been stronger than in many other countries, but markets were surprised by data suggesting the US labour market is weaker than expected and that growth may fade. Investors took this as a signal that interest rate cuts would follow and this helped bonds, property and smaller companies to perform, all of which are supported by falling interest rates.

In equity markets, companies have reported their earnings for the 3-month period to the end of June to investors. Among US companies, over half we’re doing better than expected, indicating a healthy economy, but there was concern over some of the very large businesses linked to the Artificial Intelligence investment theme. These businesses have seen their share prices appreciate rapidly over the last 18 months but despite enormous sums being invested in AI, it has not born fruit yet and revenues linked to AI have yet to come through.

UK companies did well. Economic growth has been stronger than expected and businesses are reporting that they have strong order books. The general election had little impact as The Labour Party were heavy favourites to win and the result was in line with this.

European markets posted a small gain however trailed the UK market on the back of uncertainty around French elections as well as some softer economic data points. Japanese stocks posted gains over the period although this was entirely attributed to a rally in the Yen. The Bank of Japan raised interest rates by 0.25% (the first increase since 2007), while other developed market Central Banks are poised to cut rates, this led the Yen appreciating nearly 5% against the Pound in July. Emerging Markets finished the month down as gains in India were more than offset by losses in China and Latin America.

In bond markets, investor optimism that weaker inflation in the US will lead to lower interest rates supported the performance of US government bonds. UK Gilts also performed well, but as interest rates are not expected fall as quickly in the UK, they did not quite match their US counterparts. Bonds issued by high quality businesses performed better than those of low-quality businesses.

In portfolios we continue to focus on diversification across regions to offer some protection from market volatility and to take advantage of cheaper valuations. Some of the market volatility around the end of the month may have been exacerbated by fewer buyers and sellers being active over the summer period, but we believe the fear of recession is overdone and US growth will continue to hold up, at least in the near term.

This information is intended for professional financial advisers only. Copia does not provide financial advice. This information is not intended as financial advice and should not be interpreted as such.