The infoshot to help kick-start your week

Coming up this week:

Starmer’s final GPD numbers – Thursday

The final UK GDP data from Kier Starmer’s time as Prime Minister will be released on Thursday. During his time in office, the UK economy has grown moderately by 2.3% in total, faster than all other G7 nations, aside from the US, which has grown by 3.7% in the same period.

Busy week for US economic data – Tuesday to Thursday

Trading volumes for the US market were lighter than normal last week due to a shortage of new US economic data around the 4th July holiday. This week could get busier with the release of the latest jobs, retails sales, PPI and manufacturing data.

Last week:

Farage causes yield spike

Reform UK leader, Nigel Farage’s decision to resign and hold a by-election for his Clacton-on-Sea seat sent UK gilt yields up earlier in the week. With all major parties refusing to take part, Farage will now face Count Binface, members of Monster Raving Loony Party and the Human Fox on 13 August 2026. If re-elected, the Commons Parliamentary Commissioner for Standards, Daniel Greenberg, will finish his investigation into Farage’s undisclosed £5mn “gift” from cryptocurrency billionaire Christopher Harborne. If found guilty of breaking parliamentary rules by not disclosing the gift, Clacton will face another by-election shortly after.

UK gilt yields fell on Friday after Andy Burnham’s nomination to be the Labour party leader and next PM, was backed by 322 out of 403 labour MPs. If no one else enters the contest, Burnham will be declared Labour leader this week, before taking over from Starmer on Monday 20 July 2026.

Ceasefire over in Iran

US strikes on Iran and Trump’s threat to pull American troops out of Europe spooked markets earlier in the week. The Memorandum of Understanding behind the ceasefire started to unravel on Monday after Iran attacked three commercial vessels in the Omani coast. Trump declared the ceasefire over on Wednesday, calling Iran’s leadership “scum” and “cuckoo”. Brent crude briefly touched above $80 a barrel again that day.

Overnight and this morning, Iran’s Revolutionary Guard have targeted American military facilities in Bahrain and Kuwait, hit radar systems in Oman and the Prince Hassan air base in Jordan as part of their retaliatory strikes.

This weekend, Trump rejected Iran’s claims that the Strait of Hormuz is closed off again. However, according to ship-tracking website, MarineTraffic, no commercial vessels have travelled through Hormuz with their transmitters on since yesterday evening.

More volatility in Asia

Market volatility in Asia continued from last week into trading today. In what’s being called the “black Monday sell off” by Korean media, South Korea’s main index fell nearly -9% today following another semiconductor share sell off. SK Hynix and Samsung Electronics account for more than 60% of the indexes’ market capitalization, and they saw their share prices fall -15.37% and -10.7% respectively.

Japanese reliance on imported Middle Eastern oil, meant their major index also had a volatile week following the end of the ceasefire, although the decline was less dramatic. And in today’s trading, losses in papers & pulp, communications and transport saw the market fall -1.76%.

Notice:

For regulated financial advisers and investment professionals only, Copia does not provide financial advice, and the contents of this document should not be taken as such.

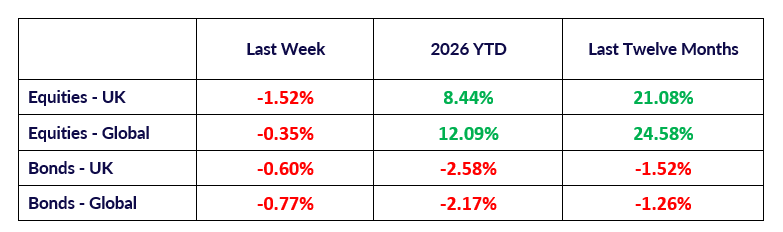

The performance of each asset class is represented by certain Exchange Traded Funds available to UK investors and expressed in GBP terms selected by Copia Capital Management to represent that asset class, as reported at previous Thursday 4:30pm UK close. Reference to a particular asset class does not represent a recommendation to seek exposure to that asset class. This information is included for comparison purposes for the period stated but is not an indicator of potential maximum loss for other periods or in the future.