The infoshot to help kick-start your week

Coming up this week:

Federal Reserve Meeting Minutes – Wednesday 8th July

Investors will scrutinise the minutes from the Fed’s latest policy meeting for clues about the future path of interest rates.

Samsung Earnings Results – Tuesday 7th July

The world’s largest memory chipmaker is projected to report preliminary operating profit of 84.3 trillion won for the quarter ended June, according to an average of analysts’ estimates compiled by Bloomberg, marking an 18-fold jump from a year ago to dwarf the company’s profit for all of 2025.

Last week:

US Job Market

US nonfarm payrolls increased by 57,000 jobs in June, missing estimates for around 110,000 and marking the softest reading since February’s fall. Prior months were also revised lower, with May’s gain cut to 129,000 from 172,000 and April’s revised to 148,000 from 179,000. The hiring slowdown was led by the biggest decline in US leisure and hospitality payrolls since 2020. The US unemployment rate ticked down to 4.2%.

AI selloff

Asian semiconductor stocks tumbled on Thursday, tracking tech losses on Wall Street after Meta’s plan, to develop a business that would sell access to AI computing power, raised worries about overcapacity. Shares of South Korea’s SK Hynix and Samsung slumped about 14% and 9%, respectively. Japan’s memory chipmaker Kioxia plunged more than 13%. The sector was also hit by concerns about rising competition and the potential impact of soaring memory prices driven by AI appetite on earnings growth and demand.

EU CPI

The rate of consumer price inflation in the eurozone fell to 2.8% in June. A reading that was lower than the 3.2% recorded in May and market expectations for 3%. Inflation slowed in some of the region’s biggest economies, including Germany, France, and Italy. Although the headline inflation rate remained above the European Central Bank’s 2% target, the latest inflation data could ease the urgency for the central bank to increase interest rates.

Notice:

For regulated financial advisers and investment professionals only, Copia does not provide financial advice, and the contents of this document should not be taken as such.

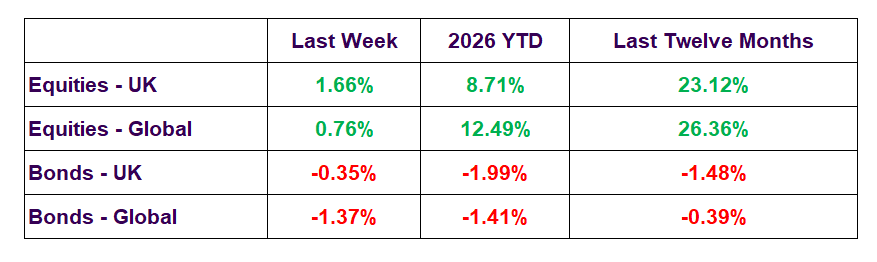

The performance of each asset class is represented by certain Exchange Traded Funds available to UK investors and expressed in GBP terms selected by Copia Capital Management to represent that asset class, as reported at previous Thursday 4:30pm UK close. Reference to a particular asset class does not represent a recommendation to seek exposure to that asset class. This information is included for comparison purposes for the period stated but is not an indicator of potential maximum loss for other periods or in the future.