The infoshot to help kick-start your week

Coming up this week:

Federal Reserve Beige Book – Wednesday

The Federal Reserve will release its next Beige Book on Wednesday. Published eight times a year, April’s edition showed mixed growth due to price pressures. With the conflict in Iran dragging on and continuing to inflate energy prices it’s likely we’ll see more murky economic conditions.

Andrew Bailey speaks – Tuesday and Thursday

The Bank of England Governor, Andrew Bailey, will speak twice this week. On Friday, in his speech delivered at the Reykjavik 2026 Economic Conference, he said the bank will continue to take a wait-and-see approach over whether the Iran war could trigger interest rate hikes.

Last week:

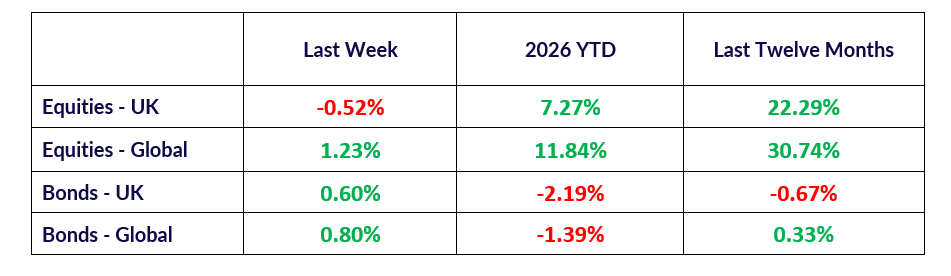

Ceasefire extension with Trump

Reports that the US and Iran were progressing towards another ceasefire extension pushed oil prices lower and buoyed US markets last week. If signed off by President Trump, the tentative agreement will extend the ceasefire by 60 days and start talks over Iran’s nuclear programme.

However, peace deal optimism took some blows over the weekend following US strikes on radar sites in Iran and Iranian missile attacks on Kuwait. Israel also stepped up their activities in Lebanon, capturing the Beaufort Castle. Today, Benjamin Netanyahu has instructed Israeli forces to bomb southern parts of Beirut. Any deal between the US and Iran will be contingent on Israel ending the fighting in Lebanon. Oil prices have risen 3.5% at the time of writing. The conflict had a major impact on the latest US Consumer Price Index (CPI) numbers which showed inflation accelerated to 3.8% in April, its highest level since May 2023. Energy costs shot up 17.9% with gasoline up 28.4% and fuel oil up 54.3%.

Japan and Korean markets continue to surge

Leading Asian markets surged again last week. Japan’s largest index rose more than 3% taking it to new highs. South Korea’s major index is now up 100% in 2026, with technology companies Micron Technology, SK Hynix and Samsung leading the way thanks to their positions in the AI supply chain. Playing a key role in the AI supply chain has helped Japan and Korea counter the disruption caused by the conflict in Iran and the closing of the Strait of Hormuz. Other South Asian countries like Singapore and Malaysia are also benefiting. They’ve seen exports of electronic goods sharply rise in the last 12 months by 46.4% and 66.7% respectively.

The AI boom is also dominating US market growth again, sending the US information technology sector up 17% in May. To put this in perspective, US materials, industrials, communication services, financials, consumer staples, utilities and energy sectors all fell between-0.01% and -4.80% during the same period.

UK markets down and Milburn interim report released

Falling house prices and energy price concerns dragged our home market down last week. According to Nationwide, average house prices fell 0.6% in May as demand was hit by the prospect of interest rate rises triggered by the war in Iran.

Recently we looked at the latest concerning UK unemployment numbers, which showed 13.5% of young people are not in employment, education or training (Neet). Following on from this, on Wednesday we saw the release of the independent interim report led by former minister Alan Milburn on young people and work. The report found that work opportunities for young people are “shrinking” at an alarming rate with one in six set to be Neet within the next five years. One million Neet young people is estimated to be currently costing the UK economy £125bn a year. The report blames the situation on the Covid pandemic, smartphones and the sharp decline in entry-level and hospitality jobs, and states that there is no evidence of a link between migration and youth unemployment.

Notice:

For regulated financial advisers and investment professionals only, Copia does not provide financial advice, and the contents of this document should not be taken as such.

The performance of each asset class is represented by certain Exchange Traded Funds available to UK investors and expressed in GBP terms selected by Copia Capital Management to represent that asset class, as reported at previous Thursday 4:30pm UK close. Reference to a particular asset class does not represent a recommendation to seek exposure to that asset class. This information is included for comparison purposes for the period stated but is not an indicator of potential maximum loss for other periods or in the future.