The infoshot to help kick-start your week

Coming up this week:

Trump peace proposal

All eyes continue to be on the conflict in Iran after President Trump called Iran’s reply to his proposed peace plan “totally unacceptable”. Earlier on last week Trump predicted that the war in Iran will be “over quickly” and said that most people understand his goal of ending Tehran’s nuclear ambitions. But Israeli Prime Minister Benjamin Netanyahu said that Iran’s stockpile of enriched uranium must be “taken out” before the war against Iran can be considered over. Trump had proposed that Iran permit shipping to pass through Hormuz while Washington ends its blockade of Iranian ports, with month-long nuclear talks to follow. Oil rose again on Monday following Trump’s social media posts.

US CPI – Tuesday

US CPI inflation is forecasted to increase from 3.3% in March to 3.7% in April, with the conflict in the Middle East adding another layer of inflationary pressures on top of the tariff shock.

Trump visit to Beijing – Wednesday to Friday

US and Chinese officials have reportedly intensified discussions to extend the current trade truce and explore potential agreements on agricultural purchases, AI safeguards, and supply chain resilience. A successful meeting between the two leaders this week could therefore provide an extra boost for Chinese equities, which have lagged their Asian peers even as regional markets rallied last month due to AI optimism and easing concerns over the Iran war.

Last week:

UK elections

Sir Kier Starmer has insisted he will carry on as prime minister despite a disastrous set of local election results for Labour which have seen his own MPs call for his resignation. Local election results showed Nigel Farage’s Reform UK making sweeping gains, while Starmer’s Labour Party lost more than half the seats it was defending, fuelling political uncertainty. The turmoil has caused 30-year UK bond yields to rise to 5.81%, their highest level since July 1998.

US nonfarm payroll data

Nonfarm payrolls in April increased for the second consecutive month, marking the strongest two-month period for nonfarm payroll increases since 2024. The US economy added 115,000 jobs, up from a forecast of 62,000, while last month’s initial print of 178,000 is now 185,000. Job gains in healthcare, transportation and warehousing, and retail were notable drivers. The unemployment rate remained at 4.3%. However, the percentage of people working or seeking work fell to the lowest level since October 2021.

Notice:

For regulated financial advisers and investment professionals only, Copia does not provide financial advice, and the contents of this document should not be taken as such.

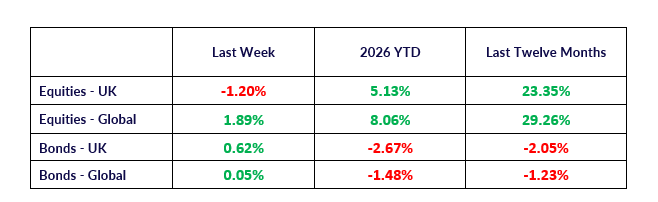

The performance of each asset class is represented by certain Exchange Traded Funds available to UK investors and expressed in GBP terms selected by Copia Capital Management to represent that asset class, as reported at previous Thursday 4:30pm UK close. Reference to a particular asset class does not represent a recommendation to seek exposure to that asset class. This information is included for comparison purposes for the period stated but is not an indicator of potential maximum loss for other periods or in the future.