The infoshot to help kick-start your week

Coming up this week:

Iran ceasefire under threat as tensions escalate

All eyes will be on the conflict in Iran after tensions escalated during the Bank Holiday weekend. Yesterday, President Trump announced operation “Project Freedom” in an attempt to help the hundreds of ships trapped in the Strait of Hormuz. Trump warned Iran’s forces they would be “blown off the face of the Earth” if they attacked US ships. Countering, Iran threatened to strike any US navy ship approaching the Strait and claimed to have struck a US frigate with missiles. This weekend, the UAE accused Iran of firing missiles into the region for the first time since the ceasefire. The ceasefire is now in its fourth week. American military have had time to restock and refuel, and if a deal can’t be reached the situation could be set to escalate.

Complicating the situation further, on Saturday, Beijing ordered Chinese companies to defy US sanctions on private refiners linked to the Iranian oil trade. China purchased more than 80% of Iran’s oil exports in 2025. Ahead of Xi Jinping’s summit with Trump later this month, Beijing appears to be taking a more aggressive stance on trade and US investments. For example, last week they blocked Meta’s $2bn purchase of AI agent developer Manus.

US payroll data – Wednesday

US payroll numbers recovered in March, climbing by 178K. Another set of strong numbers this week, combined with rising inflation, would lower the pressure on the Fed to cut interest rates this year.

Last week:

Interest rate decisions

As expected, the Bank of England, Federal Reserve, Bank of Japan and ECB all held interest rates last week. The Bank of England said further rate rises were likely due to the Iran war and its impact on energy prices and inflation. The Bank estimates average household gas and electric bills will rise from £1,641 to “close to £1,900” in July. They also think food inflation could rise to 4.6% by September.

Over in the US, Jerome Powell chaired the Fed Committee for the last time. During the press conference afterwards, he announced that he will remain on the Fed’s Board of Governors until the investigations against him and the Fed are “well and truly over, with transparency and finality”.

Big tech contributes to best month of the year while US public debt exceeds GDP

Amazon, Alphabet and Microsoft all demonstrated returns from their AI investments during their Q1 reports last week. Double digit gains were achieved in cloud computing units as the firms benefited from the intense demand for AI infrastructure. Palantir also reported sharp growth with US revenue up 133% as they try to make their AI Platform (AIP) the default option for US firms. The largely positive earnings reports from US firms have helped the largest US index record its best month since November. Meta, who don’t do cloud computing, failed to meet expectations and their plans to increase capital expenditure were met with alarm from investors. Though Meta CEO, Mark Zuckerberg, said the business was “on track to deliver personal super-intelligence to billions of people”. Meta, Microsoft and Amazon all announced or confirmed an array of layoffs as they continue to shrink their workforces.

AI spending helped US GDP rise to 2% during the first quarter of 2026. However, last week’s reading wasn’t enough to stop US public debt exceeding US annual GDP. On Thursday, the Committee for a Responsible Budget (CRFB) announced that US public debt has now reached $31.27tn, surpassing the country’s $31.22tn annual GDP. This is the first time US public debt has exceeded the size of its economy since World War Two. The nation’s gross debt, including money the federal government owes to itself, is approaching $39tn. The US is spending more servicing interest payments than it does funding defence or Medicare.

Notice:

For regulated financial advisers and investment professionals only, Copia does not provide financial advice, and the contents of this document should not be taken as such.

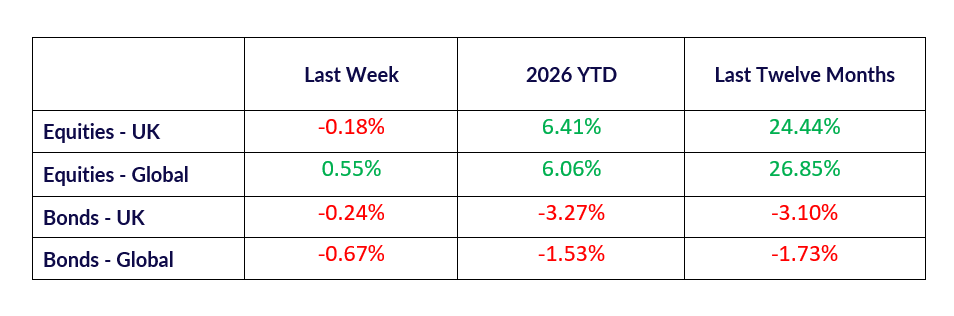

The performance of each asset class is represented by certain Exchange Traded Funds available to UK investors and expressed in GBP terms selected by Copia Capital Management to represent that asset class, as reported at previous Thursday 4:30pm UK close. Reference to a particular asset class does not represent a recommendation to seek exposure to that asset class. This information is included for comparison purposes for the period stated but is not an indicator of potential maximum loss for other periods or in the future.