The infoshot to help kick-start your week

Coming up this week:

Starmer addresses parliament about Mandelson vetting scandal – Monday

Prime Minister Sir Keir Starmer is set to address MPs this afternoon over the Peter Mandelson vetting scandal. Starmer is under pressure following the news that the Foreign Office overruled Mandelson’s vetting failure so he could become British Ambassador to the United States in December 2024. Starmer says he was not informed of the Foreign Office’s decision.

Despite calls from opposition leaders for Starmer to resign, reports suggest it’s unlikely Labour MPs will also call for his resignation. Investors will be keeping an eye on today’s statement to gauge how long-lasting and impactful the current political turmoil might be.

Kevin Warsh confirmation hearing – Tuesday

Kevin Warsh, Trump’s pick to succeed Jerome Powell as Chair of the Federal Reserve, will testify in front of the Senate Banking Committee tomorrow. His nomination must be approved by a majority of the committee before a full Senate vote.

Powell’s term is set to end on 15 May 2026. Last week, Trump threatened to fire Powell if he doesn’t step aside at the end of his term. Powell is planning to remain in his post until Warsh is confirmed in the Senate. Several Republicans have said they will block Warsh’s appointment until the criminal investigation into Powell over the renovation of the Federal Reserve office is dropped.

UK CPI (March) – Wednesday

On Wednesday, the Office for National Statistics (ONS) will release the latest Consumer Price Index (CPI) report. The data will provide an insight into the war in Iran’s impact on inflation here in the UK. The current forecast is for the annual CPI rate to increase from 3% to 3.3%.

Last week:

Positive week for markets as they ride the conflict wave

Broadly speaking, markets across the globe had a positive week following several optimistic updates about an end to the conflict in Iran, and the reopening of the Strait of Hormuz. On Wednesday, President Trump said the war was “close to over” and that during a call with President Xi, China was very happy that he was “permanently opening” the strait.

However, after being briefly reopened on Friday, the shipping route was shut again Saturday evening. The Islamic Revolutionary Guard Corps Navy (IRGCN) said it would stay closed until the US lifted its blockade on Iranian ports. Trump said the blockade will remain in place until a peace deal can be reached. Oil prices have risen in response to the closure. However, this morning Japanese markets haven’t fallen in tandem for a change as optimism around the AI sector has trumped concerns about the crisis in the Middle East.

A resolution still looks some way off. Iranian state media have reported that Iran are not planning to take part in another round of peace talks. Trump has again threatened to destroy power plants and bridges if a deal can’t be reached.

UK GDP better than expected

The latest GDP report from the Office for National Statistics (ONS) showed UK GDP increased 0.5% in February. That’s higher than the 0.1% forecast. January’s flatlining figure was also revised upwards to 0.1%. Strong performances in services and manufacturing contributed heavily to the growth.

In contrast, the International Monetary Fund (IMF) cut its growth prospects for the UK due to the knock-on effects of the Iran war. The IMF estimates that UK GDP will rise by just 0.8% this year, down from the previous forecast of 1.3%. The 0.5% cut is bigger than the downgrades for the other G7 countries.

Big US banks break records

Market volatility, and its subsequent increase in client trades, helped several major US banks post record-breaking profit numbers last week. Collectively, Bank of America, Morgan Stanley, Goldman Sachs, JP Morgan, Citi and Wells Fargo have taken in $47.4bn in profits in the first quarter of 2026

Notice:

For regulated financial advisers and investment professionals only, Copia does not provide financial advice, and the contents of this document should not be taken as such.

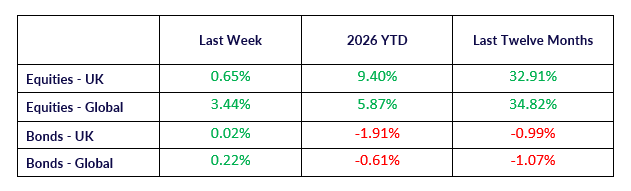

The performance of each asset class is represented by certain Exchange Traded Funds available to UK investors and expressed in GBP terms selected by Copia Capital Management to represent that asset class, as reported at previous Thursday 4:30pm UK close. Reference to a particular asset class does not represent a recommendation to seek exposure to that asset class. This information is included for comparison purposes for the period stated but is not an indicator of potential maximum loss for other periods or in the future.