The infoshot to help kick-start your week

Oil prices surge following IDF attacks on energy sites and fuel depots

The price of oil shot up above $100 a barrel for the first time since July 2022 when commodity markets opened at midnight. Energy sites and fuel depots in Iran were bombed by the Israeli Defence Forces (IDF) this weekend, covering Tehran in thick plumes of black smoke. In response, a spokesperson for Iran’s Revolutionary Guards (IRGC) threatened attacks against energy facilities in Gulf states and said, “If you can tolerate oil at more than $200 per barrel, continue this game.” According to reports, the US are unhappy about how wide-ranging the IDF’s strikes were, marking the first significant US-Israeli disagreement since the conflict began.

On Truth Social, President Trump tried to dismiss concerns about rising oil prices posting, “Short term oil prices, will drop rapidly when the destruction of the Iran nuclear threat is over, is very small price to pay for U.S.A., and World, Safety and Peace. ONLY FOOLS WOULD THINK DIFFERENTLY!”

Before the weekend’s strikes, markets were briefly boosted after the New York Times reported that Iranian Ministry of Intelligence operatives had reached out to the CIA with an offer to discuss terms for ending the conflict. However, the appointment of Mojtaba Khamenei as the country’s new Supreme Leader has squashed any optimism of a swift Iranian surrender. Khamenei, the second son of Ayatollah Ali Khamenei, has never held elected office but was seen as an important part of his father’s inner circle and has close ties with more conservative clerics and elements of the IRGC. Trump has previously said his appointment would be an “unacceptable” choice and many analysts see it as a symbolic move to show the regime will not bow to US-Israeli demands.

Earlier in the week, Trump gave Keir Starmer grief over the use of UK military bases. He also threatened to cut trade with Spain, who are currently leading the largest European economies for GDP growth, after they defied US requests to use Spanish bases in the region. The Spanish Prime Minister, Pedro Sanchez’s, outspoken “no to the war” stance on the conflict remains an outlier.

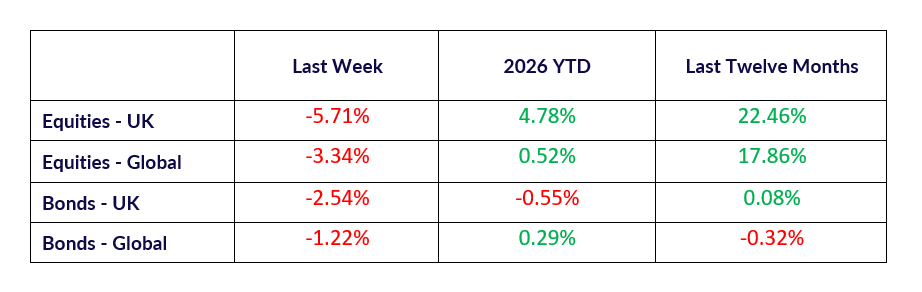

Korean markets were effectively forced to stop trading after a 12% slide last Wednesday. Korea’s dependence on oil imports from the Middle East means their economy is particularly exposed to the closing of the Strait of Hormuz. In an attempt to get ships moving again, the US International Development Finance Corporation (DFC) has set up a reinsurance scheme capable of covering losses totalling up to $20bn. In response to today’s surge in oil prices, Asian markets fell again, with Korea’s KOSPI down 5.96% and Japan’s Nikkei 225 down 5.2%. At the time of writing, UK markets are down between 1% and 2%. Global bond markets have been hit hard by the conflict as inflation fears push up yields on many of the largest economies’ bonds. Last week, UK gilts saw 10-year yields increase 0.39% and the US 10-year Treasury yield rose 0.17%. From our perspective, nothing has changed from last week and our stance remains the same: avoid knee-jerk decisions and focus on diversification.

So far, early estimates suggest the US is spending more than $1bn a day on the conflict. According to Iran’s Deputy Health Minister, Dr Ali Jafarian, at least 1,255 people were killed in Iran last week, including 200 children.

Global tariffs set to rise

Away from the conflict, US Trade Secretary, Scott Bessent said the US’s 10% global tariff will rise to 15% sometime this week. He also said he expects tariff rates will return by August to where they were before the Supreme Court’s recent ruling. The current replacement tariffs being imposed under Section 122 of the Trade Act of 1974 can only last for 150 days without an extension approved by the US Congress.

On Friday, data from the Bureau for Labor Statistics, showed the US lost 92,000 jobs in February. Healthcare, media and telecommunications, transportation and warehousing all saw downward swings. Normally these weak job numbers would increase the likelihood of Fed rate cuts, however this is effectively being counteracted by the inflation fears driven by the conflict in Iran.

Coming Up:

- Japan GDP (Q4), Monday 9 March 2026

- German CPI, Wednesday 11 March 2026

- US GDP (Q3), Friday 13 March 2026

Notice:

For regulated financial advisers and investment professionals only, Copia does not provide financial advice, and the contents of this document should not be taken as such.

The performance of each asset class is represented by certain Exchange Traded Funds available to UK investors and expressed in GBP terms selected by Copia Capital Management to represent that asset class, as reported at previous Thursday 4:30pm UK close. Reference to a particular asset class does not represent a recommendation to seek exposure to that asset class. This information is included for comparison purposes for the period stated but is not an indicator of potential maximum loss for other periods or in the future.