The infoshot to help kick-start your week

Mixed week in America as Altman and Powell spark varying market reactions

An interview with OpenAI chief Sam Altmann raised question marks about the pace of AI investments and sparked an equity sell-off last week. While comparing the current dynamic to the dot-com bubble, Altmann said, “Are we in a phase where investors are overexcited about AI. My opinion is yes. Is AI the most important thing to happen in a very long time? My opinion is also yes.” Before going on to add, “When bubbles happen, smart people get overexcited about a kernel of Truth”. US markets, particularly the NASDAQ, fell in response but did bounce back on Friday following a speech by Fed Chair, Jerome Powell.

Powell gave a major boost to the prospects of an interest rate cut in September saying, “the shifting balance of risks may warrant adjusting our policy stance”. Last week’s round of US jobless numbers was higher than expected, up 11,000 from the week before, adding more weight to cutting rates to help businesses borrow.

Any attempts to boost growth via rate cuts will have to be weighed up against inflation, but Powell was more optimistic than expected on the impact of Trump’s tariffs. Powell noted the effects on prices were now “clearly visible” and that there was a reasonable case to be made that any price rises might be “relatively short-lived”.

All eyes this week will be on chip manufacturing behemoth Nvidia when they release their latest earnings report when the market closes on Wednesday.

UK inflation and government borrowing on the rise

UK inflation is now at nearly double the Bank of England’s (BoE) 2% target. Figures for July show the UK Consumer Price Index (CPI) at 3.8%. The BoE’s latest forecast expects it to keep climbing and peak at 4% in September. Airfares were up 30.2% as airline firms cashed in on higher summer holiday demand. Food and non-alcoholic beverages were up 4.9% due to increases to the cost of beef, chocolate, coffee and fresh orange juice. Services were up from 4.7% to 5%. As a result, the Retail Price Index (RPI), which includes things like mortgage payments and insurance, also rose from 4.4% to 4.8%.

Unease over UK public finances and the stickiness of inflation sent the UK government’s borrowing costs up sharply with the interest on 30-year UK gilts rising to 5.61% – it’s highest level since May 1998. To put this rate into context, the new rate is nearly a percentage point higher than the level reached during Liz Truss’s mini-budget crisis in October 2022.

German GDP shrinks but manufacturing continues to rise

Last week’s German GDP numbers for Q2 saw Europe’s largest economy shrink by 0.3%. Q1 had been boosted by a surge in economic activity as US businesses front-loaded on German exports before the implementation of Trump’s tariffs. Over the year the German economy is now up 0.2%.

German PMI data bought some good news as it beat expectations and showed activity growing for the third consecutive month. Manufacturing posted its biggest production increase in over three years. In line with other major economies – employment has continued to decline as German firms use the rising output to go after productivity gains rather than capital expansion.

Coming Up:

- US consumer confidence, 26 August 2025 at 15:00pm

- US GDP Q2, Thursday 28 August 2025 at 13:30pm

- German CPI, Friday 29 August 2025 at 13:00pm

Notice:

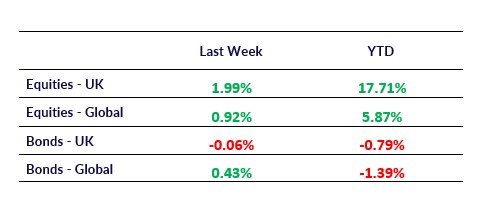

For regulated financial advisers and investment professionals only, Copia does not provide financial advice, and the contents of this document should not be taken as such. The performance of each asset class is represented by certain Exchange Traded Funds available to UK investors and expressed in GBP terms selected by Copia Capital Management to represent that asset class, as reported at previous Thursday 4:30pm UK close. Reference to a particular asset class does not represent a recommendation to seek exposure to that asset class. This information is included for comparison purposes for the period stated but is not an indicator of potential maximum loss for other periods or in the future.