The infoshot to help kick-start your week

US markets recover from “Liberation Day” while Trump encounters more setbacks

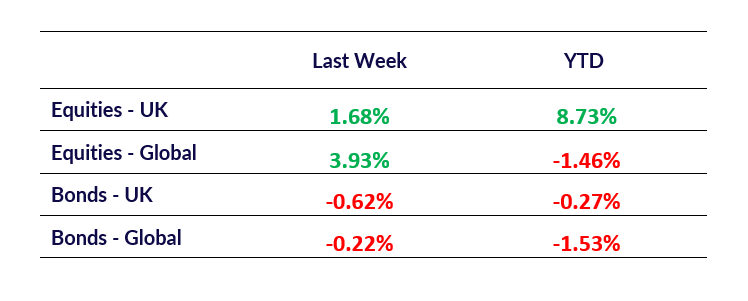

US stocks posted strong gains last week following the news that the US and China had agreed to lower tariffs and put a 90-day pause on their trade war. The agreement means US tariffs on Chinese goods will come down from 145% to 30%, and China’s levies on US imports will go down from 125% to 30% while further negotiations take place. Saudi Arabia’s Crown Prince Mohammed bin Salman also pledged to invest $600bn in the US. Details of most of the specific commitments are vague, but $142bn is set aside for arms, $20bn for AI data centres and $14.2bn for energy equipment and gas turbines. This news, combined with the tariff pause, has seen most American markets recover from their “Liberation Day” induced losses.

But it wasn’t all good news… On Friday the credit ratings agency, Moody’s, stripped the US of its triple-A rating. They downgraded the US and warned about rising levels of government debt and the growing budget deficit. US national debt now stands at $36tn and Trump’s pending “big, beautiful [economic] bill” could push the deficit higher by cutting taxes.

Trump’s signature bill, that’s based around extending tax cuts from his first term, funding mass deportations and ending tax on tips, was stopped on Friday by Democrats and right-wing lawmakers in the House of Representatives. In a major setback for Trump, republican members of the far-right Freedom Caucus helped block the bill, arguing it doesn’t make deep enough cuts to federal spending. Walmart further frustrated Trump this weekend when they announced that they expect prices to increase because of Trump’s tariffs. In response, Trump took to Truth Social to tell Walmart that he’ll be “watching” and that they should, “EAT THE TARIFFS”.

Chinese stocks rise following tariff de-escalation and Japan posts modest gains

Chinese stocks rallied following the tariff climbdowns. The deal exceeded expectations in Beijing and reportedly met all the Chinese government’s core demands. Though the rally was slightly muted as the deal appeared to reduce the prospects of a stimulus package to bolster the Chinese economy.

Japanese markets posted modest gains as the US-China deal helped lift sentiment. Negotiations between Japan and the US are still ongoing as Japanese officials continue to push for a full review and reassessment of the measures imposed by the US. GDP figures showed Japan contracted by more than expected in Q1. That contraction, the first decline in a year, was blamed on US trade tensions and weak demand from key trading partners like China.

UK market grows at fastest pace in a year

In a rare piece of good news for Reeves and Starmer, the UK economy grew 0.7% – it’s fastest pace in a year – in the three months prior to Trump’s “Liberation Day” tariffs.

According to the Office for National Statistics (ONS), growth was driven by the services sector, business investment, and net trade made a positive contribution as activity was bought forward in anticipation of Trump’s tariffs.

The UK Q1 growth numbers outstrip the US, Canada, France, Italy and Germany. However, economists at the Confederation of British Industry (CBI) warned the strength of GDP in Q1 is “likely to prove a one-off”, and both the Office for Budget Responsibility (OBR) and the International Monetary Fund (IMF) have downgraded the UK’s growth prospects in the last month.

Coming Up:

- UK Inflation Rate, Wednesday 21 May 2025 at 07:00am

- S&P Global Manufacturing PMI and Services PMI, Thursday 22 May 2025 at 14:45pm

- German GDP data, Friday 23 May 2025 at 07:00am

Notice:

For regulated financial advisers and investment professionals only, Copia does not provide financial advice, and the contents of this document should not be taken as such. The performance of each asset class is represented by certain Exchange Traded Funds available to UK investors and expressed in GBP terms selected by Copia Capital Management to represent that asset class, as reported at previous Thursday 4:30pm UK close. Reference to a particular asset class does not represent a recommendation to seek exposure to that asset class. This information is included for comparison purposes for the period stated but is not an indicator of potential maximum loss for other periods or in the future.