The infoshot to help kick-start your week

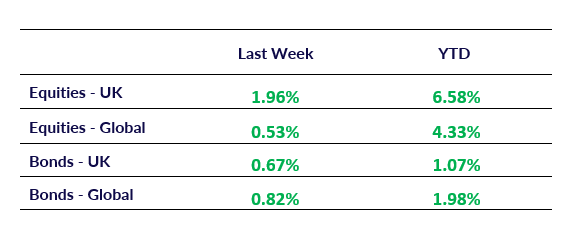

Last Week

- For nearly two years, AI technologies have driven significant gains in US equities, with the Nasdaq 100 Index rising 92% since early 2023, adding over $14 trillion in value. President Trump recently declared the US as the global AI leader, announcing $500 billion in planned investments. However, the emergence of DeepSeek, a Chinese AI startup, has disrupted this narrative. DeepSeek’s AI platform reportedly matches top US models at a fraction of the cost and energy consumption. This development caused a major selloff in US tech stocks, with the Nasdaq 100 falling 3% on Monday, erasing nearly $1 trillion in value. Nvidia experienced its worst day since March 2020, losing almost $600 billion in market value. The sudden shift has raised questions about the profitability of massive AI investments and the justification for high valuations of mega-cap stocks, which now make up 30% of the S&P 500’s weighting.

- The Federal Reserve has maintained its current interest rate range of 4.25%-4.5%, signalling a cautious approach to monetary policy. Fed Chair Jerome Powell emphasized that the central bank is not rushing to lower rates, citing a strong economy and stable labour market. The unanimous decision reflects the Fed’s desire to see further evidence of cooling inflation before making any adjustments. Powell noted that while inflation remains somewhat elevated, the economy continues to show resilience. The central bank is particularly interested in evaluating the potential impact of President Trump’s policies on immigration, tariffs, and taxes. The Fed’s stance suggests they will wait for more comprehensive economic data before considering rate cuts, with Powell specifically mentioning the need for “serial readings” indicating sustained inflation progress. This measured approach comes after a series of rate reductions in late 2024, demonstrating the Fed’s commitment to carefully managing monetary policy in a complex economic landscape.

- Europe’s stock market is experiencing a resurgence, with the Stoxx Europe 600 Index up 6.6% in January, outperforming the S&P 500’s 3.2% gain. This marks the best monthly performance for European stocks in two years. The rally is driven by solid earnings, expectations of ECB rate cuts, and a potential reprieve from immediate US tariffs. European equities, long considered undervalued, are attracting investors due to their lower valuations compared to US stocks. The Stoxx 600 trades at 14 times estimated earnings, significantly lower than the S&P 500’s 22 multiple. This valuation gap, combined with the ECB’s ongoing rate cuts and potential economic growth, makes European stocks increasingly attractive. Despite challenges such as lack of tech giants and political uncertainties, Europe’s market is benefiting from reduced exposure to AI-related risks and potential US-China trade tensions. As a result, investors are reconsidering their allocations, with some experts suggesting a shift towards European and Japanese bank stocks.

Market Pulse

Coming Up

- UK BoE Interest Rate Decision, Thursday 6th February 2025 at 12:00pm

- US Nonfarm Payrolls, Friday 7th February 2025 at 1:30pm

- US Unemployment Rate, Friday 7th February 2025 at 1:30pm

Notice:

For professional advisers only, Copia does not provide financial advice, and the contents of this document should not be taken as such. The performance of each asset class is represented by certain Exchange Traded Funds available to UK investors and expressed in GBP terms selected by Copia Capital Management to represent that asset class, as reported at previous Thursday 4:30pm UK close. Reference to a particular asset class does not represent a recommendation to seek exposure to that asset class. This information is included for comparison purposes for the period stated, but is not an indicator of potential maximum loss for other periods or in the future.Open document settingsOpen publish panel