The infoshot to help kick-start your week

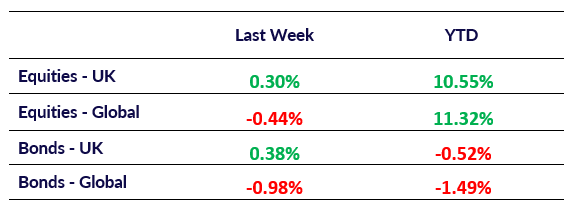

Last Week

- San Francisco Federal Reserve President Mary Daly has indicated that it may soon be appropriate for the Federal Reserve to consider lowering interest rates. Daly’s comments align with recent remarks by Fed Chair Jerome Powell, who noted at the Jackson Hole symposium last week that he is increasingly confident inflation is returning to the Fed’s 2% target. Powell suggested that a potential adjustment in monetary policy could be forthcoming as inflation stabilises. In parallel, there are emerging dynamics in global markets. Analysts, including Stephen Jen, CEO of Eurizon SLJ Capital, suggest that as the U.S. contemplates rate cuts, Chinese companies could respond by selling a significant portion of their U.S. dollar-denominated assets. This could potentially strengthen the yuan by up to 10%. Jen also highlighted currency risk as a critical factor that may not be fully reflected in current market valuations, with the yuan possibly playing a more prominent role moving forward.

- Crude oil prices have eased slightly following a significant three-day rally—the sharpest since April last year. Brent crude futures have dipped today but continue to trade above $80 per barrel, supported by ongoing concerns over potential disruptions to Libyan supply. Market sentiment remains cautious as geopolitical tensions in the Middle East persist, keeping traders on edge. In Europe, developments also pose risks to energy markets. Ukraine reported that Russia launched over 100 missiles and nearly as many drones in a widespread attack on Monday, targeting power infrastructure. The strikes caused widespread blackouts and resulted in civilian casualties.

- The challenges facing China’s economy continue to weigh on global markets. A recent announcement from a major Chinese e-commerce company provided a cautious outlook, signalling concerns over the country’s economic health. The news sent shockwaves through markets, reflecting growing investor anxiety over China’s slowing recovery. These concerns extend to the commodities sector, where a leading global miner has warned of near-term volatility driven by China’s uneven economic performance. Excess steel production has put pressure on prices, and iron ore supply is likely to exceed demand into next year. Recent corporate data from China highlights the difficulties, showing deepening losses at steel mills, raising the prospect of additional production cuts to stabilise margins in the struggling industry.

Market Pulse

Coming Up

- US CB Consumer Confidence, Tuesday 27th August 2024 at 3:00pm

- US GDP (Q2), Thursday 29th August 2024 at 1:30pm

- EUR CPI Data released, Friday 30th August 2024 at 1:30pm

- US Core PCE Data Released, Friday 30th August 2024 at 1:30pm

Notice:

For professional advisers only, Copia does not provide financial advice, and the contents of this document should not be taken as such. The performance of each asset class is represented by certain Exchange Traded Funds available to UK investors and expressed in GBP terms selected by Copia Capital Management to represent that asset class, as reported at previous Thursday 4:30pm UK close. Reference to a particular asset class does not represent a recommendation to seek exposure to that asset class. This information is included for comparison purposes for the period stated, but is not an indicator of potential maximum loss for other periods or in the future.Open document settingsOpen publish panel